How to Trade Binary Options 8: Money Management & Probability

Most binary options discussions spend too much time on entry signals and not enough time on the questions that decide whether a trader is still around to use those signals next month. How do you risk manage, and do you increase your ability to stick to your risk management routine even when emotions run high?

An essential part of risk management is how much is being risked on each trade, i.e. staking rules. Many inexperienced traders gloss over this part and go by their gut, and that also helps explain why so many new retail binary options trading accounts are wiped out without ever becoming profitable.

Staking rules do not feel very exciting, and they do not flatter the ego. They are plain, mechanical, and often a little annoying. Unfortunately, they also matter more than most retail traders want to admit. To some, they are essentially an insult. The trader wants to feel like the smart one; the person who can think on their feet and make the right decision in the heat of the moment instead of being bound by silly and rigid staking rules. And these accounts typically need constant money refills to remain active because they never become profitable over time.

In binary options, money management is especially important because the payout structure for a conventional retail binary option is asymmetric. The trader risks 100 percent of the stake hoping to make something less than 100 percent in profit. Even a decent strategy can be damaged by poor sizing, and a weak strategy can be destroyed at impressive speed by aggressive staking. A few bad entries are survivable if the sizing is small. A few bad entries at the wrong size are not.

Probability calculations and the need for account survival need to be treated as part of the trading method, not as a separate chapter that’s added on only for overly cautious people. Every binary trader is already making probability decisions whether they understand the math or not. The only real choice is whether those decisions are explicit and disciplined, or emotional and expensive.

Proper money management in binary options is not about maximizing excitement or recovering losses quickly. It is about giving a real edge, if one exists, enough room to appear without allowing ordinary variance to wipe out the account first. Several different methods have been developed to help with this, and we will look at some of the more widely known ones below, including flat staking, percentage staking, the Kelly criterion, and Martingale escalation. Flat staking offers simplicity, while percentage sizing offers adaptation. Kelly helps frame the relationship between edge and optimal size, though full Kelly is usually too aggressive for real trading. Martingale should be avoided as it offers a quick route to impressive account damage.

Here’s where you are in our 10-step guide to trading binary options:

- The Foundations of Binary Options

- Regulatory Landscape and Safety

- Market Analysis I – Fundamental Drivers

- Market Analysis II – Technical Charting

- Technical Indicators for Binary Options Trading

- The Three Pillars of Binary Options Strategy

- Timeframes & Expiry Management

- Money Management & Probability

- The Psychology of Binary Trading

- Advanced Implementation & Tax Compliance

Why Money Management Matters More in Binaries Than Many Traders Understand

First and foremost, when you decide to use binary options, you give up many of the other risk management tools that we use in non-binary trading. Money management therefore becomes even more important.

It is important to remember that conventional binary options compress outcomes. Each trade settles as a fixed win or a fixed loss. That structure means that the distribution of results is less flexible than for non-binary trading, e.g. stock trading and forex trading. A spot forex trader can, for instance, cut a loser early (manually or through a stop-loss order), take profit early, scale a winner, or hold for an outsized move that offsets several smaller losses. Conventional binary options usually offer far less room for that. The payout is capped, the loss is the full stake, and the clock decides when the trade ends.

When you lose 100% of your stake on each losing position, position sizing becomes extremely important. If a trader risks too much per contract, a short losing streak can wipe out the account or cause damage that is mathematically very hard to repair. As always, it is important to remember the math. After losing 50 percent of your account, you do not need a 50 percent gain to recover, you need 100 percent. Lose 75 percent, and the account now needs 300 percent just to get back to where it started. The market is not kind enough to adjust the difficulty level after a bad week.

Another reason money management matters more in binaries is the seductive speed of the product. Retail binary options platforms tend to push ultra-fast binary options heavily, i.e. those that are intraday. When contracts settle quickly, it creates a constant opportunity to fall into bad patterns, such as increasing size after losses, chasing recovery, or convincing oneself that “just one decent winner” will restore balance.

There is also a psychological trap built into fixed payout products such as binary options. Since the exact possible loss is known in advance, traders often feel safer than they should. They think in terms of “I can only lose this stake” while ignoring how many times that stake can be repeated in one session or one emotional spiral. Fixed risk per trade is not the same as controlled risk across behavior. If the stake is too large relative to the account, the risk is still too large, even if you know beforehand exactly how much you stand to lose.

A sensible trader therefore starts with the assumption that survival comes first. Growth matters, of course, but growth is only meaningful if the account can endure losing streaks, poor weeks, and ordinary randomness without the trader being pushed into desperate behavior.

Building a Staking Framework Focused on Survival

A practical staking framework for binary options does not need to be complicated, but it needs to be durable. For a beginner, that usually means risking a small fixed percentage of capital per trade, keeping the size consistent across similar setups, and reducing or pausing trading when results suggest the edge may not currently be present.

For many traders, a risk level somewhere around 1 percent to 2 percent per trade is conservative enough to survive ordinary losing streaks while still allowing growth if the system has merit. Some traders may use less. Very few should use much more, whatever the last few trades have done to their confidence.

Below, we will look into flat sizing, percentage-based sizing, and position sizing based on edge. Flat sizing can help simplify, while percentage-based sizing can help adapt naturally to growth and drawdown. Position sizing based on edge is a bit more complicated, but it can help with understanding if taking the risk is even worth it.

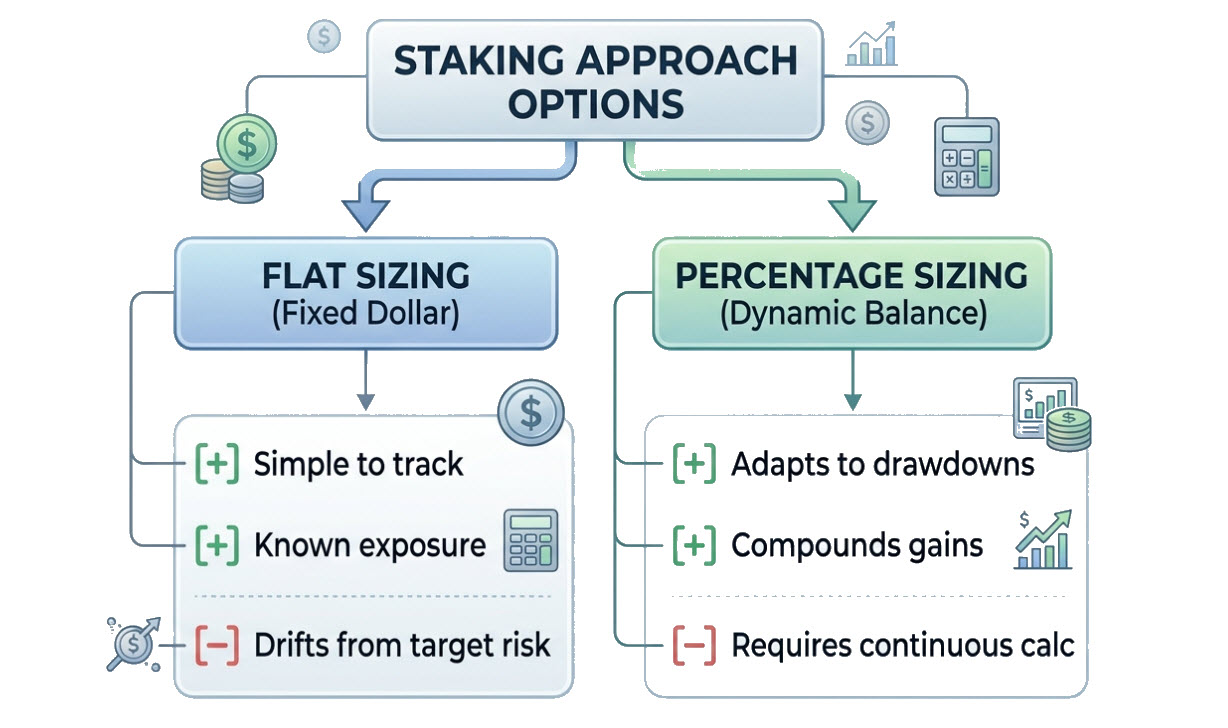

Flat Sizing vs. Percentage-Based Sizing

Once a novice trader moves past the fantasy that each trade deserves whatever size feels emotionally satisfying, they often settle into one of two broad approaches.

- The first is flat betting, where the same fixed amount is risked on every trade.

- The second is percentage based sizing, where the stake changes with account size.

Both can work, and both have their strengths and weaknesses. The main point is that both are generally superior to random size changes driven by recent wins, recent losses, or sudden inspiration.

Flat Staking

Flat staking is simple. If the trader decides each trade will risk $20, then every trade risks $20 until the rule is deliberately revised. The attraction is clarity and simplicity. Results are easy to track, and the emotional load is low because the stake does not change every time the account moves. For newer traders, this simplicity can be useful because it keeps the focus on strategy quality rather than on constant recalculation.

In binary options, flat staking also makes the effect of the payout structure easier to see. If every trade risks the same amount, the trader can observe a clear result over time without the noise of changing stake size. This makes it a practical method for early testing and for traders who value consistency.

The weakness is that flat staking does not adapt to account size. If the account grows, the fixed stake becomes proportionally smaller, which slows compounding. If the account shrinks, the fixed stake becomes proportionally larger, which increases the risk of wiping out the account. A trader risking $20 on a $2,000 account is risking 1 percent. Risk the same $20 after the account has fallen to $1,000 and you are now risking 2 percent. This is not fatal, though it means flat staking works best when the trader reviews size periodically rather than leaving it unchanged forever. Otherwise the system can drift away from the intended risk level.

A routine should be put in place for revising the stake size and its relation to the account balance. Without a firm routine and rules to follow, you risk starting to make emotional changes in the heat of the moment.

Percentage-Based Sizing

Percentage-based sizing continuously adjusts stake size relative to the current account value. If the rule is to risk 2 percent per trade, then a $2,000 account risks $40, while a $1,500 account risks $30. This approach has an important advantage. It scales down automatically during drawdowns and scales up during growth. That means losses reduce future exposure and wins allow gradual compounding without the trader needing to revise the stake size manually every few sessions.

Some platforms contain tools that can be used to easily calculate the stake size based on how much of your account balance you have decided to risk per trade.

For binary options, percentage-based sizing is often the cleaner long-term approach because it respects survival. A trader using 1 percent or 2 percent risk per trade can lose several contracts in a row without catastrophic account damage. That does not make losing streaks pleasant, but it does keep them in the category of manageable rather than account ending.

There is also an important psychological benefit. Percentage models reduce the temptation to “make it back quickly” because the size contracts after losses. The account forces a quieter tone, and that is useful in a product where emotional escalation is common and usually expensive. Of course, only risking 1% per individual trade will not prevent an emotional trader from suddenly opening 100 trades at once, or doing 100 trades in very quick succession. To prevent these types of overtrading, you need to have additional rules in place, and the fortitude to stick to them.

The weakness of percentage sizing is mostly behavioral, not mathematical. Traders become impatient because growth looks slower at conservative risk levels. They then raise the percentage, usually at exactly the wrong time, or start overriding the rule after losing runs. The method itself is sound. The troubles begin when mood overrides discipline.

The Kelly Criterion and Position Sizing From Edge

The Kelly Criterion is one of the most discussed formulas in position sizing because it tries to answer a simple question with actual mathematics: given an edge, how much of capital should be risked to maximize long-run growth?

The appeal is obvious. Traders want a rational framework for sizing, and Kelly seems to offer one. The danger is that many people hear the phrase, like the sound of it, and then use a rough version of it to justify betting more than they should.

At its core, Kelly is not a system for bravery. It is a sizing method based on probabilities and payoff ratios. It assumes the trader has a measurable edge, knows the odds well enough to estimate it, and is willing to tolerate the volatility that comes with growth-oriented staking. In binary trading, those assumptions are already under pressure because estimating a stable edge is hard enough before adding short-term noise, shifting payouts, and platform risk. The underlying idea behind the Kelly Criterion is relevant to binary options, but with important caveats that make it much less reliable in practice than in traditional trading.

What Kelly Is Actually Measuring

Kelly tries to maximize the logarithmic growth of capital over a large number of repeated bets. In plain English, it is asking: if this opportunity can be taken again and again under roughly similar conditions, what fraction of the bankroll gives the best long-run growth without betting so much that the account becomes fragile? That is an elegant question, and Kelly gives an elegant answer, though elegance does not guarantee practical comfort.

For a simple bet, the Kelly fraction can be written as:

f* = (bp − q) / b

Where f* is the optimal fraction of capital to risk, b is the net payoff ratio, p is the probability of winning, and q is the probability of losing, which is 1 − p.

This formula matters because it links sizing directly to edge. If the edge is small, Kelly size is small. If there is no edge, Kelly tells you not to bet at all. If the edge is negative, the formula produces a negative result, which is a polite mathematical way of saying this is not a good habit. That last point is worth slowing down for. Many retail traders size positions as if they have an edge simply because they have a setup. Those are not the same thing. A setup is a pattern or rule. An edge is a positive expected value over a meaningful sample after costs, imperfections, and human behavior. Kelly assumes the second one, not the first. If the trader does not really have a true edge, only an imaginary one, Kelly is being applied to fiction.

Why Kelly Is Harder To Apply In Binary Options

Kelly only works well if you genuinely know your edge, probabilities are stable, outcomes are independent, and payoff odds are fair and transparent. Binary options often violate several of these.

Unfavorable payout structure

Most retail binary options platforms pay around 70–90% on wins while losses are 100%.

That means you need a surprisingly high win rate just to break even.

This is how we calculate the break-even probability:

pbreak−even=11+bp_{break-even}=\frac{1}{1+b}pbreak−even=1+b1

This means that for binary options where the payout is 80%, you need to be correct roughly 55.6% of the time to just break even. Any less than that, and your trading is costing you money.

So you need about 55.56% accuracy just to have zero expected value before accounting for costs such as slippage and platform issues. If those frictions exist (which they can do), your required win rate is actually a bit higher than 55.6% to break even. And at break-even, Kelly will recommend zero sizing. So for Kelly to actually recommend you stake any money, your accuracy needs to be even higher, and this is notoriously difficult for short-term binary options.

Estimating Edge is Extremely Difficult

Kelly is highly sensitive to estimation error. If you think your edge is 60%, but it is actually 55%, then full Kelly becomes dangerous and can rapidly destroy capital. Binary options amplify this because payouts are asymmetric and short-term variance is huge.

Even among non-binary traders, many of the experienced ones will not use full Kelly. Instead, they use half Kelly, quarter Kelly, or certain capped exposure rules, to give their account more room for estimation errors.

Binary Options Have “All-or-Nothing” Volatility

Unlike stocks where partial adverse movement still leaves capital invested, binary options settle to either the fixed payout or the full stake loss. This creates larger drawdowns and higher psychological pressure.

Kelly assumes you can survive volatility long enough for edge to manifest, but in binary options, streaks can become brutal and quickly wipe out an account even when the overall strategy does have a real edge.

Using Kelly for Binary Options Trading

Kelly can still be useful in binary options as a framework for thinking about edge, a warning against overbetting, a way to scale down after poor expectancy, and a mathematical upper limit on risk. But using full Kelly sizing in binary options is usually considered too aggressive. Instead, we can use a quarter Kelly, and combine it with maximum daily drawdown limits and volatility-adjusted sizing.

Let’s take a look at the example above, where the binary options had a payout ratio of 80%. If a broker pays 80 percent on a winning trade, then b = 0.8. If the trader’s estimated win probability is 60 percent, then p = 0.6 and q = 0.4.

We plug this into the formula:

f* = (0.8 × 0.6 − 0.4) / 0.8

f* = (0.48 − 0.4) / 0.8

f* = 0.08 / 0.8 = 0.10

That suggests risking 10 percent of capital per trade under full Kelly if the trader really has a 60 percent win rate at an 80 percent payout. On paper, that is the growth optimal fraction. In practice, for binary trading, it is very aggressive.

Take another example. Suppose the payout is 70 percent and the true win rate is 58 percent.

Then:

b = 0.7

p = 0.58

q = 0.42

f* = (0.7 × 0.58 − 0.42) / 0.7

f* = (0.406 − 0.42) / 0.7

f* = -0.014 / 0.7 = -0.02

The result is negative. That means a 58 percent win rate is not enough at a 70 percent payout. The trader does not have a positive Kelly bet. This is one of the useful things Kelly forces into the open. It does not care whether the setup feels good. Kelly is useful as a diagnostic tool even for traders who never use the exact fraction in live trading. It forces the trader to think in terms of actual edge rather than vague confidence. A trader with a 55 percent strike rate might sound competent in casual conversation. In binary options, that number may be unprofitable depending on payout. Kelly exposes that without involving ego and emotions.

Why Full Kelly Is Usually Too Aggressive in Practice

As we have already touched on above, full Kelly is considered too aggressive by many traders, especially within the field of binary options. Even if a trader can estimate their edge honestly, full Kelly is often too aggressive for real-world trading when account survival is a priority. The reason is simple. Kelly maximizes long-run growth, but it also produces large swings in equity. Those swings are difficult in practice, especially for a new hobby trader who might not have sufficient capital at their disposal to handle wide swings.

Even if your gut feeling tells you to go full Kelly, please remember that market conditions shift and win rate estimates are often based on fairly limited historical samples. A trader may believe their system wins 60 percent of the time, but the true forward rate may be lower once market regime changes, execution errors appear, and emotional mistakes compound under pressure.

This is why many serious traders who think in Kelly terms use fractional Kelly, such as half Kelly or quarter Kelly. If full Kelly suggests 10 percent, half Kelly would mean 5 percent and quarter Kelly 2.5 percent. That reduction sacrifices some theoretical growth in exchange for lower volatility, lower drawdown severity, and better survival odds if the edge was overstated. In real trading, that is often a good bargain.

There is also a behavioral reason. A formula that looks rational on paper can become irrational in the hands of someone who will abandon it after a losing streak (or after a surprisingly great streak). Full Kelly is only useful if the trader can endure the drawdowns it creates. Many cannot, particularly in binaries where losses arrive as full stake losses and where contract frequency amplifies the emotional aspects of trading. A smaller fraction that the trader can actually follow is worth more than a larger one that will be abandoned the moment the account starts bleeding or the trader feels overly optimistic.

Kelly, then, is best treated as a framework for thinking about edge and risk, not as a command to size aggressively just because the formula says so. In binaries, the more honest use of Kelly is often to prove that the account should be risked less, not more.

Understanding the Kelly Criterion Background

The Kelly Criterion was developed in 1956 by John Larry Kelly Jr., a scientist working at Bell Labs, one of the most influential industrial research centers of that era. Bell Labs was originally the research and development arm of the U.S. telephone monopoly AT&T, created to advance telecommunications technology. Over time, it became a place where academic-level science met real-world engineering at a massive scale, and it ended up shaping much of modern computing and communications.

What made Bell Labs special is that it wasn’t just a corporate engineering department; it functioned more like a world-class scientific institute inside a company. Researchers there worked on both fundamental science and practical engineering problems, and this explains why someone at Bell Labs would work on betting and trading systems. It sounds odd at first, but at Bell Labs, problems were often framed in very abstract, mathematical terms, and “how to stake” was really just a model for a deeper question. How should we allocate limited resources under uncertainty? The original niche for Kelly’s work was not gambling or investing, it was about information theory and telecommunications research, as Kelly was working on problems related to signal transmission and noise in communication channels.

John Larry Kelly Jr. introduced what we today know as the “Kelly criterion” in a paper titled “A New Interpretation of Information Rate”, published in the journal of the Institute of Radio Engineers. The key insight was that there is a mathematical similarity between transmitting information efficiently through a noisy channel and growing capital efficiently under uncertainty. Kelly showed that if a bettor has a statistical edge, there is an optimal fraction of capital to wager that maximizes the logarithmic growth rate of wealth over time. A major feature of Kelly sizing is that it explicitly balances aggression (growth) against survivability (drawdown risk).

The Kelly criterion became famous outside the world of telecommunications research when gamblers started using it in horse racing and blackjack. Eventually, it reached investors who applied it to portfolio management and trading. It was largely Edward O. Thorp who brought the Kelly criterion into the world of casino gambling. He was a mathematician and a pioneer of quantitative investing who helped bridge probability theory, gambling strategy, and modern finance. Later, Warren Buffett and Charlie Munger would also discuss ideas closely related to Kelly-style capital allocation.

All this might feel like meaningless trivia to a retail trader eager to jump into binary options trading, but we have elected to include it in our article to show that the Kelly criterion is not just some random idea about position sizing that sounds good but does not have research to back it up. This does not mean that the Kelly criterion is the only worthwhile method for position sizing, but it does mean that prospective traders can scrutinize it in a scientific way to understand its usefulness for maximizing long-term compounded growth while avoiding ruin.

Why the Martingale System Keeps Blowing Up Retail Trading Accounts

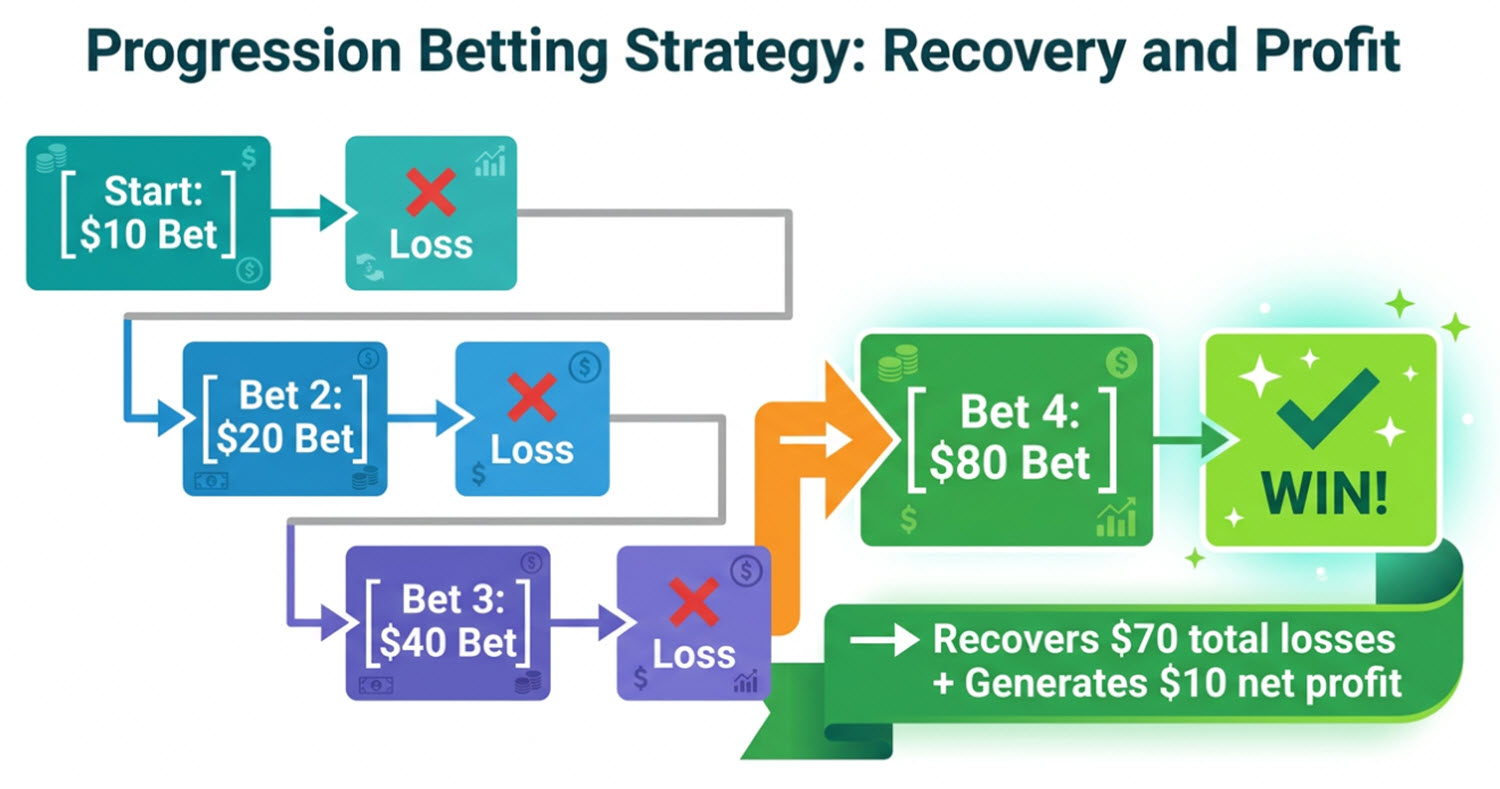

Martingale deserves direct treatment because it remains one of the most persistent myths in retail binary trading. The idea is simple enough: after each loss, increase the next stake so that one win recovers all prior losses and produces a net profit. On paper it looks clever because the binary outcome appears tidy and the trader imagines that a winning trade must arrive before the sequence becomes untenable.

The problem is that Martingale assumes 1:1 payouts, infinite capital, no stake limits, no emotional strain, and a system that can survive long losing streaks. Real accounts usually run without those luxuries. A streak of losses does not need to be extreme to become destructive once position size starts doubling or rising aggressively.

The Martingale system was used on the roulette table long before retail binary options platforms existed. For bets such as red/black, high/low, and even/odd that pay 1:1 when you win, the idea is to double the stake after each loss, and let the first win recover all previous losses, plus give you a small profit equal to the original stake.

Example:

- Bet $1 → lose

- Bet $2 → lose

- Bet $4 → lose

- Bet $8 → win

Total lost for the three first wagers: $1 + $2 + $4 = $7

Win on an $8 bet at even odds gives $8 profit, so net gain is $8 minus $7 = $1. The profit is $1, which is the same as your original wager.

Now, one of the problems with using Martingale for binaries is that the system was developed for bets that pay 1:1 (e.g. red/black at the roulette table). With binaries paying less than 100% of your stake, you need to adjust the stake size accordingly to actually cover previously lost stakes. This makes the Martingale system more complicated to use with binaries and it also means that the stake size will rise even quicker, since you need to increase by more than 100% for the system to work.

Consider a roulette player starting with a $10 stake and doubling after each loss. The sequence goes $10, $20, $40, $80, $160, $320, $640. After only six losses in a row, the next required trade is already large relative to what you stand to gain. In binaries, where a losing trade loses 100 percent of the stake and a winning trade may return only 70 to 90 percent in profit, the escalation is even quicker. The classic Martingale logic was not designed for a payoff structure where wins do not return an even amount relative to losses. To compensate, the binary options trader has to increase stakes even more aggressively than simply doubling.

Example:

- You are using binaries where the payout is 80%. This means that if you risk $1 and win, you get $1.80 back, and you have made $0.80 in profits.

- You start with a $10 stake, and your target profit for the cycle is therefore $10. This means that your goal is to recover all previous losses from the cycle and make a $10 profit.

- If you get seven losses in a row, the stake progression will look like this: $10, $25, $56.25, $126.56, $284.77, $640.72, and $1,441.63. As you can see, you are quickly risking very large amounts of money, hoping to make a meagre $10 profit. If you lose the $1,441.63 stake, the next binary option in the cycle would require a $3,243.66 stake.

With a small hobby trading account, it is easy to see how losses can escalate faster than the account can tolerate. Martingale relies on you being financially able to increase the stake as many times as required before you finally get a win, and if you can’t do this, the system will collapse after a string of losses. It also relies on your counterpart accepting unlimited wagers.

The Martingale method feels safe because most short sequences do contain a winner somewhere. But then a longer losing streak arrives, and the account is quickly wiped out.

Prime Number Staking Systems

Within the worlds of both trading and gambling, you can encounter a selection of different stake sizing systems based on prime number series. While they vary from each other, their core is the belief that correlating your stake sizes to a series of prime numbers will increase your chances of becoming profitable.

A number is a prime number if it has exactly two distinct positive divisors: 1 and itself. That means a prime number cannot be evenly divided by any number other than 1 and itself without leaving a remainder. The first twenty prime numbers are therefore 2, 3, 5, 7, 11, 13, 17, 19, 23, 29, 31, 37, 41, 43, 47, 53, 59, 61, 67, and 71. (1 is not a prime number, since it has only one divisor, not two.)

A prime number stake size system will place trades using a sequence of prime numbers, e.g. 2, 3, 5, 7, 11, 13, and so on. Depending on the exact system, this might mean increasing or varying your stake according to primes, or only trading on steps that correspond to prime-numbered positions in a sequence. It can sound sophisticated because primes are an interesting part of mathematics, and inexperienced traders can easily get the impression that there is some hidden beneficial structure or intelligence behind the method.

In reality, though, using prime numbers in this way does not create any trading edge or help manage position sizes in a meaningful way. Whether you bet 2, 3, 5, or 11 units does not influence the probability of the next trade being a win or loss. The market does not “respond” to your staking pattern, and it does not contain exploitable patterns linked to prime numbers.

What systems like this actually change is not your probability of winning, but the volatility of your results. Because prime numbers increase irregularly, your stake sizes will also increase in an uneven way. This can create the illusion of a “method” or “progression”, especially during short winning streaks, but over time, it usually leads to the same mathematical reality. If your trades do not have a genuine statistical edge, your expected return is negative, regardless of how you sequence your bets. And a system that keeps increasing bet size will help you deplete your account balance even faster.

This is where many retail traders get misled. A structured betting pattern can feel like risk management, but it is not the same as having an edge or controlling risk in an advantageous way. In fact, uneven stake scaling can make risk harder to perceive, and that can lead to rapid drawdowns that feel surprising even though they are statistically normal.

By contrast, approaches like the Kelly Criterion are based on estimating whether you actually have an edge and then sizing positions according to that edge and your bankroll. Percentage-based position sizing is about surviving fairly long losing streaks by always keeping individual stakes low in relation to the account size. Fixed-size stake systems means keeping stake size fixed, instead of being swayed by emotions or arbitrarily increasing or decreasing stake sizes based on some type of mathematical sequence (prime numbers, Fibonacci, etc.).

The prime number system changes the pattern of your stake sizes, but it does not change the underlying odds. Still, systems based on prime number sequences remain popular among inexperienced traders due to a combination of psychological reasons. Humans are wired to look for patterns, and a structure like prime numbers gives a feeling of order, like there is a hidden logic behind your stake sizes. That sense of order is emotionally satisfying. Secondly, these systems often survive because they are easy to remember and easy to apply. Actually finding out your edge and doing Kelly calculations require more effort than following a system such as Martingale, Prime Numbers, or Fibonacci. That simplicity can feel like discipline, but discipline only helps if the underlying logic is valid.

Prime number staking can look good over a short-term sample, e.g. when you backtest it against historical market data in demo mode. When someone applies a structured betting pattern during a lucky period, it can look like the system is working. When you test over a short period of time, it is easy to mistake short-term variance for proof of concept. The notion becomes even stronger since there is a powerful psychological pull toward “mathematical sounding” methods within the trading community. Primes, Fibonacci sequences, The Golden Ratio, and other famous mathematical ideas carry authority. This creates an illusion that the method is grounded in science, even when it has no connection to probability theory or expected value. These systems often spread through social reinforcement rather than verification.

If someone posts a profitable cycle and chalks the success up to prime sequence stake sizes, others copy it. For a social media guru eager to convert likes into ad-link sign-ups, it is tempting to refrain from showing how a prolonged losing streak wiped out the account. Over time, you get selection bias, where successes are visible and failures take place behind the scenes. The key point is that popularity in trading communities is not the same as validity. Even a deeply flawed staking system can feel structured, look mathematical, and even produce short-term success purely by chance.

Gambler’s Ruin and the Mathematics of Account Death

Gambler’s ruin is the idea that a player with finite capital, facing repeated bets, eventually goes broke if the game continues long enough and the odds are not favorable enough. More specifically, a player with finite capital, repeatedly betting in a game with unfavorable odds against an opponent with effectively unlimited capital, will eventually go broke if play continues indefinitely.

The reason this matters in binaries should be obvious by now. The payout structure favors the house (the trading platform), and ultra-short-term contracts can entice a trader to burn through their balance quickly. A trader does not need to be reckless in a dramatic sense to face ruin, they only need to risk too much relative to the edge and then keep trading through normal variance.

Losing Streaks Are Normal, Not Rare

It is important to take into account that losing streaks are normal, not rare. We like to think about them as unusual; a very strange bout of really bad luck. In reality, they are not.

If a trader wins 55 percent of the time, that still means they lose 45 percent of the time. Over a long enough sample, sequences of four, five, six, or more consecutive losses are not freak events, they are part of the normal landscape.

Inexperienced retail traders often size positions as if the recent win rate guarantees near term smoothness. That is a mistake. Probability does not arrange outcomes in a friendly order. A system with a positive expected value can still deliver ugly streaks. If the account is not sized to survive those streaks, the trader may not last long enough for the edge to reassert itself.

In binary options, this is even more severe because each loss is usually a full stake loss. There are no partial stop-outs softening the sequence. When traders say “my system stopped working”, the account statement often translates that more accurately as “my sizing assumed a smoother path than reality delivered”. Inexperienced traders have a tendency to assume that they will always get a win soon enough to save their account from depletion. In reality, losing streaks can be brutal and go on for much longer than what an inexperienced trader “feels” is realistic.

Risk of Ruin in a Negative or Fragile Edge System

If the system has a negative expected value, risk of ruin is not really a possibility to be managed, it is the destination, only the timing varies. Conservative sizing may delay the outcome, but it does not change the fundamental drift. Retail binary trading tends to combine negative expectancy with fast, aggressive trading, and it comes as no surprise that a very high number of new retail binary options accounts never become profitable. The account is being pulled downward by the math and the process is accelerated by large stakes (in relation to the account size) and frequent trading.

With that said, a positive system can also face high ruin risk if the edge is small or fragile, and the trading style uses large stakes (in relation to the account size). A fragile edge can, for instance, be one that depends on specific market conditions, precise execution, or a narrow window of behavioral discipline. Many retail systems are fragile in exactly this way. The trader believes they have a durable advantage, though the advantage may shrink or disappear once live trading conditions replace tidy backtests. This is why successful survival-based money management strategies usually assume the edge estimate may be wrong, or at least less stable than hoped. Smaller sizing is not pessimism; it is admission that uncertainty exists not only in the market, but in the trader’s own measurement of skill.

The uncomfortable truth is that many traders blow accounts not because they had no chance, but because they sized as if uncertainty had already been conquered. The market tends to correct that belief quickly.