How to Trade Binary Options 2: Regulatory Landscape and Safety

Regulation matters more in binary options than many beginners assume. On a binary options platform, your broker is typically not a broker in the conventional sense. You are not being connected to other traders on a market. Instead, the platform takes the opposite side of each trade. When you profit, it comes out of the platform’s bottom line. When you lose money, it lines the pockets of the platform. This set-up is not necessarily a bad thing, but it does create a built-in conflict of interest that must be managed well, and it makes independent supervision and auditing extra important.

The company that is in charge of the binary options platform is in charge of that entire universe and it is easy for a sketchy firm to manipulate the platform to benefit itself. In much of the retail binary options market, the platform is also the price source, the settlement mechanism, and the custodian of client funds, all while also taking the other side of each trade. That makes regulatory quality a direct trading variable rather than a background legal detail.

Regulation and trader protection must be treated as part of market mechanics and not as an afterthought. Where the contract sits, who controls settlement, and what protection exists if something goes wrong, can have a huge effect on your bottom line. A dodgy broker can do much more damage than a weak strategy.

Regrettably, it has become difficult for retail brokers to find binary options platforms based in supervised jurisdictions with strong trader protection rules. This is because most of those jurisdictions have banned brokers from selling retail binary options. As a consequence, the brokers who want to remain active on those markets have moved to very lax jurisdictions. From lax jurisdictions, they can continue to market and sell binary options to retail traders in banned jurisdictions without getting into trouble locally. That does not mean that every binary options firm based in a lax jurisdiction is fraudulent or even low-quality. In fact, we’ve identified and listed top-rated binary options providers, some of which are based overseas. It means that traders from stricter jurisdictions will not enjoy the level of trader protection that they may be used to from back home.

Here’s where you are in our 10-step guide to trading binary options:

- The Foundations of Binary Options

- Regulatory Landscape and Safety

- Market Analysis I – Fundamental Drivers

- Market Analysis II – Technical Charting

- Technical Indicators for Binary Options Trading

- The Three Pillars of Binary Options Strategy

- Timeframes & Expiry Management

- Money Management & Probability

- The Psychology of Binary Trading

- Advanced Implementation & Tax Compliance

The Global Regulatory Hierarchy in 2026

From a retail trader protection perspective, the 2026 regulatory picture is best understood as a hierarchy rather than a single standard. At the top are jurisdictions where retail trader protection is strong, and where retail derivatives distribution is heavily supervised, product design is constrained, and investor protection rules are backed by active regulators who both supervise firms and enforce the existing rules. For many traders, this gives peace of mind, but there are also those who dislike it when it means certain products become out of reach, leverage is heavily capped, welcome bonuses are banned, and negative account balance protection is mandatory.

Then, there is a second tier of jurisdictions where retail binary options are not banned nor heavily restricted, but general trader protection rules and broker supervision are still in place. These jurisdictions are not against trader protection; they have just decided that retail traders should be allowed a bit more freedom to make their own mistakes.

Below, we find the laissez-faire jurisdictions where trader protection and broker supervision are really weak or non-existent. Many of the firms that want to continue selling retail binary options on markets where the practice is banned are based in one of these jurisdictions, since they do not want to risk being in a second-tier jurisdiction where authorities might cooperate with foreign financial authorities or take umbrage with a licensed local firm that is deliberately violating the rules of other countries.

The 2026 binary options market is defined by these different levels. In stricter jurisdictions, the sale of retail binaries is banned or heavily restricted, e.g. by being pushed into exchanges (USA) or by banning short-term retail binaries (Canada). In the laissez-faire jurisdictions, the trader will get weaker firm supervision, poor access to recourse, and generally not enjoy that safety net that stricter financial authorities try, albeit imperfectly, to provide.

That does not make every retail trader foolish or every retail broker fraudulent, but understanding this dynamic is necessary to accurately assess counterparty risk for different retail binary options venues.

Examples of Different Regulatory Approaches Around the World

So the hierarchy is fairly blunt. In top-tier jurisdictions (in terms of retail trader protection) such as the US, UK, EU, and Australia, the sale of retail binaries is either banned or channeled into regulated exchange frameworks instead of independent broker platforms. The practical result is that a large share of global retail binary activity now sits outside those top-tier systems. That is the reality check. Traders often hear the word “global” and imagine a broad, mature, internationally harmonized market. What they usually face instead is a fragmented patchwork where strict jurisdictions no longer license the product and laissez-faire jurisdictions host the bulk of the surviving retail supply.

As a trader, the first step is to find out exactly what your own legal situation is. Local binary options regulation, tax treatment, and consumer law all matter. From a safety perspective, it is also best to avoid situations where your own legal system will not be able to help you if a broker turns out to be sketchy. If you pick a broker based in a jurisdiction that is not your own, you should assume weaker recourse from the outset. You are introducing jurisdictional complexity, and that comes with its own set of risks and challenges.

Check the legal status of binary options in different countries at a glance.

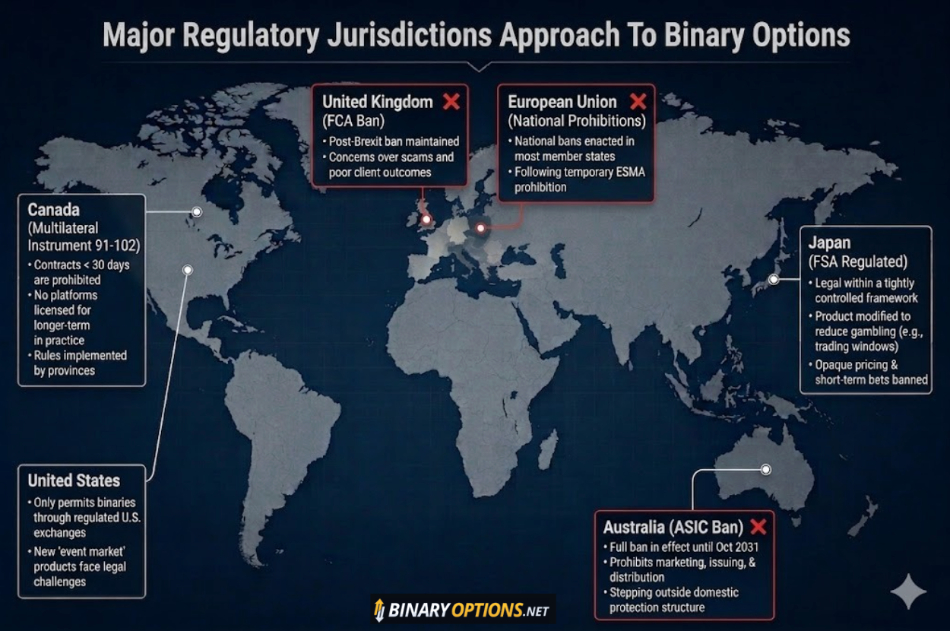

Retail Binary Options in the United States

The United States only permits binaries when they are offered through a regulated U.S. exchange that holds the correct permit, as articulated in our binary options guide for US traders.

A lot of things are currently happening on the U.S. market, as so-called event market platforms are moving in with products that are eerily similar to binary options. There are several ongoing legal cases right now, especially pertaining to contracts based on the outcome of sporting events, since national online platforms are coming head-to-head with state-regulation in this field. There is also the issue of offering what essentially comes down to betting on the outcome of elections.

Retail Binary Options in Australia

In Australia, ASIC banned the marketing, issuing and distribution of binary options to retail clients with effect from May 3, 2021. After conducting a review, ASIC concluded that binary options had resulted in, and were likely to continue to result in, significant detriment to retail clients in Australia.

The ban is a product intervention order that needs to be renewed regularly to stay in effect, but there are currently no signs of it not being renewed. The current product intervention order is in effect until early October 2031.

This means that there are no retail binary options platforms and brokers licensed by ASIC. The market is effectively closed in retail form. Any Australian user accessing binaries through a foreign platform is stepping outside the domestic consumer protection structure.

Retail Binary Options in the European Union

In 2018, the European Securities and Markets Authority (ESMA) temporarily prohibited the marketing, distribution, and sale of binary options to retail traders in the European Union. The temporary prohibition was put in place to protect retail traders immediately while giving the membership countries time to enact their own national regulations.

When the membership nations had enacted their own rules, ESMA stopped renewing the temporary ban. Today, most EU member countries prohibit the marketing, distribution, and sale of binary options to retail traders.

Retail Binary Options in the UK

When ESMA enacted the temporary ban in 2018, the UK was still a member of the EU, and it became one of the first countries to put a national ban in place. After Brexit, the UK FCA confirmed that its ban on the sale of binary options to retail consumers would stay in place even post-Brexit.

Like many other financial authorities, the UK Financial Conduct Authority (FCA) is not only concerned about poor client outcomes from the product itself; it also wants to keep consumers away from an industry saturated with scammers. This combination is a main reason why binary options are banned or severely restricted for retail traders in so many countries.

Retail Binary Options in Canada

In Canada, retail binary options are effectively shut down, but the way this is done is a bit more nuanced than a simple blanket ban. The key rule comes from the Canadian Securities Administrators (CSA) through what’s called Multilateral Instrument 91-102. This rule prohibits the sale of binary options to retail traders if the contract has a term of less than 30 days.

Retail binary options with expiries longer than 30 days are not banned, but the seller still needs to hold the appropriate license to offer them in Canada. In practice, retail binary options platforms tend to be focused on short-term contracts and are unwilling to go through the process of obtaining a Canadian license when it would still only give them permission to sell long-term contracts. As of our latest checks, there are no platforms licensed in Canada to offer binary options to retail investors.

The regulatory structure in Canada helps explain why the outcome looks this way. Canada does not have a single national securities regulator. Instead, authority is divided among provincial regulators. These bodies are the ones that actually create and enforce securities law within their respective jurisdictions. The CSA is not a regulator itself, but a coordinating organization that develops harmonized rules and policies, which each province then adopts into its own legal framework.

So when the CSA introduced the binary options restrictions, each province implemented them locally, giving the policy nationwide effect without creating a federal law. Provinces have the power to go further if they choose, and an individual province could, for instance, decide that 60 days is the limit instead of just 30 days.

Retail Binary Options in Japan

In Japan, retail binary options are legal, but only within a tightly controlled regulatory framework. They are classified as financial derivatives and fall under the supervision of the Financial Services Agency (FSA), which means they are treated as part of the formal financial system.

Only firms that are properly licensed in Japan are allowed to offer binary options to retail clients. These are typically established domestic financial institutions that also belong to industry self-regulatory bodies such as the Japan Securities Dealers Association. Because of this structure, there are legitimate, regulated providers operating in the country.

What makes Japan especially distinctive is not just that binary options are allowed, but how heavily the product itself has been modified by regulation. The authorities did not simply permit the standard high-speed, all-or-nothing contracts that are common globally. Instead, they imposed design constraints intended to reduce gambling-like behavior. Extremely short-term bets (shorter than a few hours) are not permitted, and trading is organized into set windows rather than continuous, rapid-fire execution. Pricing must be transparent, with firms showing probability-based values and bid–ask spreads instead of opaque fixed payouts. Returns are also constrained so that the payoff structure is more balanced and less prone to extreme outcomes.

These rules are paired with broader investor protection measures, including disclosure requirements and limits on how aggressively firms can market the products. At the same time, the Japanese regulator actively blocks or warns against offshore platforms that try to target local residents without authorization, reinforcing the idea that binary options must stay inside the licensed domestic system.

The overall result is a model where retail access is permitted, and there are legitimate providers, but the product has been reshaped into something closer to a standardized, lower-volatility derivative. In contrast to the U.S., which focuses on restricting binaries to regulated exchanges, Japan allows broker-based offerings but tightly controls the structure and behavior of the contracts themselves.

Understanding Counterparty Risk

With binary options, counterparty risk is chiefly the risk that the firm on the other side of your trade, and the holder of your funds, cannot or will not perform their duty to you. When you use a binary options platform based in a lax jurisdiction, this is not a secondary risk; it is one of the main risks.

It is important not to confuse market risk with counterparty risk. Market risk is the risk that your trade idea is wrong. Counterparty risk is the risk that the venue itself becomes the problem. Traders are used to talking about the first one because it feels like trading. The second one feels like unimportant paperwork until it isn’t.

Both risks can end up costing you a lot of money and should be taken seriously. A trader should think about counterparty quality long before thinking about strategy optimization. There is no point shaving a few basis points off entry quality in theory while ignoring whether the venue itself can be trusted to settle, custody, and pay out profits and withdrawals.

Counterparty Risk Associated With Insolvency

If a broker mismanages hedging, takes concentrated exposure, loses banking support, faces a surge in withdrawals, or has their company accounts frozen by the legal authorities, traders may discover that their broker can no longer honor withdrawal requests. This is why strict financial authorities that take trader protection seriously impose a list of broker requirements intended to reduce the risk of insolvency and increase the chances of traders getting their money back even if the brokerage company becomes insolvent.

This list typically includes capital requirements, mandatory segregation of client funds, and various other conduct rules, and there will also be mandatory reporting to the financial authority.

Client Money Segregation

Mandatory (and actually enforced) client fund segregation is one of the first things to look for, though it needs careful reading. Segregation means client money is held separately from the broker’s operating funds. In stronger regulatory systems, this is often tied to formal client money rules. In lax jurisdictions, the requirement is either absent or not actually supervised and enforced. The requirement can exist on paper, but without meaningful supervision behind it.

The absence of mandatory and enforced segregation is a warning sign because if the firm becomes insolvent after co-mingling your money with their own, you no longer have a strong claim to that money. Instead, you only have a general claim, and you will be fighting with all the other creditors to get your piece of anything that might remain as the firm folds. Typically, traders get nothing or very little back from this type of bankruptcy proceeding when their funds have been co-mingled.

Investor and Trader Protection Schemes

In many top-tier and mid-tier jurisdictions, the government has established investor and trader protection schemes that can step in, up to a certain amount, if a locally licensed broker fails to honor their obligations due to insolvency. Typically, it only becomes relevant when a firm has broken the rules by co-mingling client funds with company funds.

To be eligible for compensation, you will typically need two things:

- The firm you are using must be authorized to be a broker in that jurisdiction.

- You need to be a resident of the jurisdiction.

Examples:

- Mary lives in the UK, but is using a binary options broker based in the Seychelles. The broker is not licensed by the UK FCA. Mary’s money is not covered by the UK scheme because the broker is not authorized to be a broker in the UK.

- Peter lives in Uganda and is using a broker based in Kenya. The broker holds a Kenyan license. Peter’s money is not covered by the Kenyan scheme because he is not a Kenyan resident.

This type of governmental investor and trader protection scheme can drastically reduce counterparty risk, but only if you are actually covered by it. Many of the popular jurisdictions for retail binary option firms do not have this type of scheme, or the cap for maximum payment is really low.

Counterparty Risk Associated With Fraud or Refusal to Honor Contracts

As we covered earlier, your “broker” is actually your counterpart in each trade when you use a standard retail binary options platform online. This is not automatically a problem, but it does mean that your profit is their loss and your loss is part of their revenue stream. This creates a built-in conflict of interest.

A good broker may manage that conflict through internal controls, stable pricing, clear settlement rules, hedging, and general risk management. A dishonest broker may manage it by leaning on opacity and by taking every advantage that the platform structure allows, including fraudulent manipulation of price feeds and expiry times.

The conflict matters most when markets get messy. During high volatility, a broker may struggle more with its own risk management, but also have more room to justify delayed execution, altered early exit pricing, widened effective dealing costs, or unusual settlement references.

Financial authorities have warned users repeatedly of unsupervised binary options platforms manipulating trading software to distort outcomes for customers. That is not the same as saying every binary options broker in a lax jurisdiction does so, but it is enough to establish that the risk is real, known, and severe enough to feature in formal regulator warnings.

Some fraudulent brokers do not even bother to manipulate the platform; they simply freeze your account from withdrawals and make up bogus excuses for a while before they start ignoring your attempts at communication. In a jurisdiction with strong trader protection rules, you can report this broker to the financial authority and have them investigate the situation. In a lax jurisdiction, you can’t count on much help from the legal system.

Exchange Trading As a Way To Reduce Counterparty Risk

As mentioned above, the United States has adopted an approach where binary options are legal, but only when traded on U.S. exchanges that hold the correct permits for binary options. The U.S. is thus making a clear distinction between exchange trading and over-the-counter (OTC) trading, and this has a lot to do with reducing counterparty risk.

In an exchange model, the contract sits within a formal trading and clearing framework. Rulebooks are public, contract design is standardized, and the market structure is not built around a private broker deciding every operational detail behind the curtain. That does not remove trading risk, but it does change who controls the mechanics and under what oversight they operate.

In the OTC retail model, the broker usually sets the strike price, defines the payout, controls the platform, controls the price feed, acts as the custodian of the trader’s money, and acts as the market maker. The trader is not entering a neutral marketplace in the same sense because the trader is dealing with a private counterparty under that firm’s terms, technology, and enforcement culture. Some firms are more transparent than others, but the structural difference remains. The venue is not simply matching buyers and sellers; it is warehousing or economically taking the trade.

Exchange-style products and OTC binaries can look similar at a distance. Both are defined outcome contracts with capped loss and fixed payout, but the operational risks are not the same, especially not when it comes to counterparty risk. In an exchange framework, disputes, settlement methods, and clearing obligations sit within a stronger public structure keenly supervised by a financial authority.

In an offshore OTC framework, disputes often run into private terms, foreign jurisdictions, limited compensation routes, and the practical problem that the same firm controlling settlement may also be the party with something to lose when you win. A trader who ignores that difference is not comparing products properly.

Counterparty Risk and Access To Actual Recourse

If the firm you are using freezes your account from withdrawals, manipulates your account balance, throws bogus charges at you, or manipulates the price feed or expiry time to turn a winning trade into a loss, you want to be able to report them to a legal system that actually has teeth.

You also want the path to be accessible and straightforward. If you are dealing with a broker in a lax jurisdiction, you might not get much help from the financial authority. Instead, you may be required to hire local legal representation to open up a civil case against the broker. When a broker is located on the other side of the world, and you might not even speak the local language, this becomes an uphill battle before it has even started. Sketchy and fraudulent brokers know very well that the typical small-scale retail trader does not have the resources to fight them, especially not when the jurisdiction is deliberately lax when it comes to trader protection.

Specific Warnings

The Bonus Trap

If you have seen adverts for binary options brokers that accept clients globally, you have probably also seen promises of huge welcome bonuses.

Example: Deposit $1,000 today, immediately receive another $1,000 in bonus funds, and trade with more capital.

The offer looks very appealing, and many inexperienced traders jump on it without looking at the fine print, especially the turnover requirement (also known as trading requirement). You accept the bonus, do some profitable trading, try to make a withdrawal, and are told that no withdrawal is allowed until a large multiple of the bonus, or of the deposit plus bonus, has been traded.

You thought the bonus was extra flexibility. In practice, it became a lock on the account. When you complain, you are just referred to the fine print of the agreement you approved when you accepted the bonus terms and conditions.

A reasonable approach for traders is that any feature making withdrawals harder than making deposits should be read with suspicion. Plenty of expensive lessons start with a “reward” that was never really meant to be yours.

Also, don’t throw good money after bad. Brokers frequently encourage traders to make additional deposits to unlock a frozen account. Don’t fall for it.

Predatory “Account Managers”

Any type of aggressive sales tactics or solutions that could weaken your control over your account (trading decisions, account money, or both) should be seen as a warning sign. The managed account offer is one example. A broker employee, “senior analyst,” or “account manager” offers to trade for the client or guide every trade in real time. In serious markets, that raises immediate questions about authorization, suitability, conflicts, and responsibility.

In the lax jurisdiction binary space, it happens without any checks and balances in place. The platform wants the deposit, wants trading volume, and wants the client dependent on the broker contact rather than on their own decision process. Once that pattern starts, pressure to top up the account often follows, and the sales tactics can be both aggressive and manipulative.

Technical Safety, Custody, and Account Security

Technical safety is not glamorous, which is probably why many traders neglect to think about it until something breaks. A broker handling funds and identity documents should meet at least basic operational standards, and failure to do so is a big red flag.

Account security matters. Multifactor authentication helps prevent unauthorized access by requiring a second verification method. For a trading account holding money and personal documents, 2FA should be treated as basic hygiene, not a premium feature. A platform that does not offer it is behind even ordinary consumer finance standards and should not be trusted with your money and identification documents.

SSL encryption belongs in the same category. It does not prove honesty, but it is part of minimum technical competence. More broadly, traders should look at withdrawal authentication, device login alerts, password controls, and whether the broker’s legal entity, support contacts, and dispute channels are easy to identify. This should be done before money is deposited or you part with any identification documents. If the platform is vague on custody, vague on security, and vague on complaints, treat that as a warning sign.

The main point is that a binary options platform is not just a trading platform; it is also a money handling and identity handling system, and traders who judge it only by the payout ratio for 2-minute contracts are taking huge risks that go far beyond market risk.

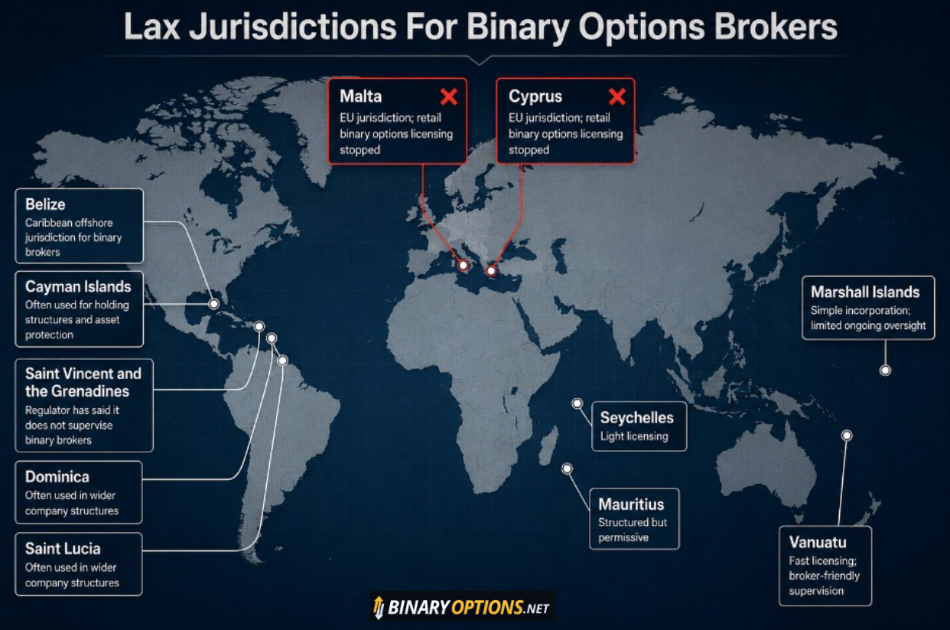

Examples of Popular Jurisdictions For Retail Binary Options Platforms

If you’re looking at where retail binary options platforms tend to be based, the pattern is pretty consistent globally: they cluster in jurisdictions where they will be lightly regulated, and a few jurisdictions show up repeatedly. If you dig a little deeper, you’ll often find rather intricate company structures that involve more than one of these jurisdictions, to make legal accountability even more difficult.

One example of a popular location is the Seychelles. It has a financial regulator and a licensing regime for financial services firms, but the requirements are relatively low. Many binary options firms are incorporated there because it allows them to operate internationally while not facing stringent product restrictions or intrusive auditing. The Seychelles also looks good for platforms that want access to the growing African retail binary options market, since the Seychelles is a member of the African Union and the Southern African Development Community (SADC).

Binary options firms targeting African retail traders are also increasingly using Mauritius, another island nation that is a member of both the African Union and the Southern African Development Community (SADC). Mauritius offers a more structured licensing framework than the laxest jurisdictions, while not imposing any retail binary options ban. For retail traders in parts of Africa where retail binaries aren’t regulated at all, a firm licensed by Mauritius can feel like “the least bad” choice.

If we move westward, we run into several popular jurisdictions in the Caribbean, such as the Marshall Islands, Saint Vincent and the Grenadines, and Belize. There are also nations here that company groups use as a part of their wider setup, but more commonly for holding companies and asset stashing rather than basing their main client-facing binary options firm there. Examples of such countries are the Cayman Islands, Dominica, and Saint Lucia.

The Marshall Islands are popular among online brokers because of simple incorporation procedures and limited ongoing oversight. It is attractive to brokers who want flexibility rather than strict supervision. The same can be said for Saint Vincent and the Grenadines. Notably, the local regulator here has explicitly stated that it does not regulate and supervise forex or binary options brokers in the way traders might expect.

In the South Pacific Ocean, roughly 1,750 km (1,100 miles) east of northern Australia, we find a small island nation named Vanuatu. To supplement its meagre incomes from small-scale farming and limited tourism, the nation has began positioning itself as an offshore location for financial services companies, including retail binary options firms. Company licensing can be obtained in a matter of months, capital requirements are modest, and firms are not always required to maintain a substantial physical presence in the country. This makes it fast and cost-efficient for brokers to set up operations aimed at global clients.

The Vanuatu Financial Services Commission does supervise licensed entities, but it is known for taking a very broker-friendly, hands-off approach, and it does not offer the kind of trader and investor protection mechanisms you would see in stricter jurisdictions.

What About Cyprus and Malta?

Cyprus and Malta used to be important hubs for retail binary options firms, but both countries are a part of the European Union, and both of them have stopped licensing retail binary options firms.

If a retail binary options firm is claiming authorization from CySEC (Cyprus) or the Malta Financial Services Authority (MFSA), they are either making that up out of thin air or using a license number that has not been valid in a very long time.

Fraudsters Using Binaries as a Lure to Bring in Victims

Regrettably, the popularity of binary options has made them a very popular lure for fraudsters. These fraudsters are also aware that retail traders in strict jurisdictions can pick a locally licensed broker. As traders look outside the strongly regulated frameworks, they are more likely to end up in the clutches of fraudsters.

Several different types of scams exist that involve binary options, and it is a good idea to learn how to spot early warning signs. Below, we will look at a few common types.

Fraudsters Only Looking For Your First Deposit

These scams can be pretty crude because all the fraudster needs to do is lure you into making that first deposit. Then, the gig is up, and you have lost your money, but at least the loss is limited.

Fraudulent Binary Options Platforms That Know How To Play The Long Game

These platforms are much more harmful because they know how to milk traders dry. They are fully functioning binary options platforms, with all the bells and whistles. Things will typically go very well at first (sometimes because the platform is manipulated to keep you happy), and you will be confident in your ability to trade and eager to make bigger deposits. You will probably even be able to make a few small withdrawals without friction, and this will reinforce the idea that you are in the hands of a serious firm.

Then, the problems start. Suddenly, the price feed gets weird when you have a big stake at risk. Independent sources show you a winning price point, but your platform claims you lost.

Or, you do a series of winning trades, build your account balance, and feel great. Then, you try to make a bigger withdrawal, and run into a brick wall. For whatever made-up reason, your account is frozen. You will then be coaxed into making additional deposits to unlock it. The broker knows fully well how difficult it is for us to admit we have been defrauded and walk away from the money. We are much more likely to keep jumping through their hoops for a while, always believing that THIS deposit will be the one that actually resolves the problem.

Examples of common excuses are temporary system errors, unexpected compliance reviews, tax prepayments, insurance fees, account unlocking charges, withdrawal method verification, or minimum turnover conditions that were not obvious at the deposit stage.

Personal Data Harvesters – Beware Of The Risk Of Identity Theft

Your deposit is not the only thing at risk. It can be tempting to think that if you only do a $100 deposit, you can’t possibly lose more than $100.

The problem is the account verification and know-your-customer (KYC) checks. Reputable brokers based in strict jurisdictions do them, so when the platform starts asking for documentation, we take that as a positive sign. But you are handing over your identification documentation to fraudsters.

Anything you hand over to prove your own identity and residency can be used by a scammer pretending to be you. You are running the risk of identity theft, and your name can even show up in criminal investigations down the line, when the fraudsters have assumed your identity while defrauding others.

Clone Sites Are On The Rise

The clone broker problem is not unique to binaries; it is a problem for all reputable trading sites these days. A clone firm is not merely an unregulated broker. It is a scam operation that copies the identity markers of a real, regulated and reputable firm in order to use its good name. It has become very easy to copy a whole website and place it on another domain name. The copied material may include everything, including all the right details when it comes to specifics such as company name, address, logo, license number, website language, certificates, and customer documents. Only a few things will be different to ensure you send your money to an account controlled by the fraudster or to make sure you don’t contact the real customer support.

The first practical defense is direct register verification. If a broker claims to be authorized in the UK, verification should start with the official FCA register. If it claims Australian licensing, the ASIC professional registers search should be used, and so on.

The important point is not the existence of a number on the broker’s site. It is whether that number, legal entity, and business activity match the regulator’s own system. Then, and this is important, you have to follow the link to the official broker site posted in the registry. Otherwise, you are just confirming a name and license number stolen by the scammer, and still ending up on the fraudulent site.

Sophisticated scammers will happily serve you a bunch of lies if you reach out to ask why the domain they promote is different from the official domain. Instead of using the official BrokerXYZ.com, you should use BrokerXYZVIP.com to get special VIP privileges. Since you live in India, you should use BrokerXYZ-India.com to make sure you are onboarded through the entity that is compliant with Indian law. And so on.

Just like many other scammers, clone brokers and related frauds often lean on urgency. The target is pushed to deposit quickly, approve a “verification” payment, hand over remote device access, or speak to a “senior account manager” right now. They do not want you to have any time to do independent checks or discuss the offer with a friend who might raise some questions. Real financial services firms can be annoying in many ways, but working really hard to whip up a blind panic within you is usually not their modus operandi. Pressure to act quickly is information. It tells you that the other side needs you to act right now, before you have time to think and investigate.

Watch Out For Recovery Scams

If you fall victim to a financial trading scam, it is important to stay vigilant and understand that you are now a likely target for a recovery scam.

A recovery scam is a follow-up fraud that targets people who have already lost money to a scammer. Instead of offering an investment opportunity, the scam begins with your loss. The scammer contacts you, claiming they can recover your funds, trace stolen money, or force a broker to refund you through legal, technical, or regulatory channels.

They often present themselves as lawyers, cybercrime investigators, blockchain tracing specialists, or representatives of foreign regulators or law enforcement. They can pretend to be associated with well-known institutions like the FCA, BaFin, SEC, FBI, or Interpol, often backing this up with fake documents or convincing websites. This creates an illusion of legitimacy even though there is no real connection to those organizations.

A key part of how these scams operate is something sometimes called a “suckers list”. This is essentially a database of people who have previously lost money to scams. The original fraudsters can sell your info to another scammer if they do not feel like doing the recovery scam themselves. Information can also be harvested from public forums and similar places where you have shared your experiences. Once someone appears on such a list, they can be repeatedly targeted by different fraud groups over time. The database can be extensive and include information about not only who you are, but also exactly how much you lost, to which platform, and so on. This makes the recovery scam so convincing because it makes sense to believe that only law enforcement or similar would have all this information, or that you have been contacted by a very skilled hacker who is actually capable of doing blockchain reversals.

The effectiveness of recovery scams also comes from psychological manipulation. The scammers exploit the emotional state of someone who has already suffered a financial loss. After a loss, people often experience frustration, regret, and a strong desire to “fix” the situation. They can also be embarrassed in front of others and feel a deep urge to be the one who resolves the issue. Scammers take advantage of this by offering hope and framing themselves as the solution.

Just like most other scams, recovery fraudsters like to create a false sense of urgency. They will claim that funds have been seized and are about to be released, that legal windows are closing, and that immediate action is required, which pressures victims into acting quickly without verifying the claims. Self-proclaimed blockchain recovery experts can state that some complex technical update is about to take place that will make recovery impossible, or that cryptocurrency is about to be tumbled and lost forever unless we act right now, without delay.

The goal for recovery scammers is to extract payments from the victims. You will be told you must pay fees for legal processing, taxes, verification, transfer costs, blockchain gas, etc. Each payment is framed as the final step before releasing the recovered funds, but the cycle continues until the victim realizes the con or runs out of money.

Ultimately, recovery scams work well because they combine hope with authority and urgency, while targeting people who are already vulnerable from a previous financial loss. The safest assumption is that any unsolicited offer promising to recover lost trading funds for a fee is itself part of a second scam rather than a genuine recovery effort.