How to Trade Binary Options 10: Advanced Implementation & Tax Compliance

Trading Is Only Half the Job

Most retail traders spend almost all of their energy on the front end of the activity. Charts, setups, news, timing, indicators, entry, and so on. Those things matter a lot, obviously, but they are only half the work. The other half sits in the back office: record keeping, reviewing, tax administration, proof of funds, broker documentation, etc. That is the dull but necessary work that separates a short-lived hobby from something more long-lasting and serious that can survive in a legal and financial context.

Advanced implementation in binary options is not a matter of adding more indicators or inventing more dramatic setups. It is about building the administrative parts of the operation that make your trading survive scrutiny. You need both internal scrutiny to stay on the profitable path and a method for keeping records in a way that is accepted by the relevant governmental authorities who carry out external scrutiny.

For the internal scrutiny, a habit of backtesting, journaling, and documenting decisions will help turn memory into evidence that you can evaluate. For the external scrutiny, proper record keeping and correct tax treatment are essential. Things such as audit ledgers, reconciled records, and legal due diligence can be worth their proverbial weight in gold. You will need clean records and enough legal and tax hygiene to ensure that profits, if they arrive, do not vanish in an administrative chaos afterwards. So, this part of our article series is less about entries and exits and more about administration and evaluation.

Here’s where you are in our 10-step guide to trading binary options:

- The Foundations of Binary Options

- Regulatory Landscape and Safety

- Market Analysis I – Fundamental Drivers

- Market Analysis II – Technical Charting

- Technical Indicators for Binary Options Trading

- The Three Pillars of Binary Options Strategy

- Timeframes & Expiry Management

- Money Management & Probability

- The Psychology of Binary Trading

- Advanced Implementation & Tax Compliance

Internal Scrutiny: Let Backtesting And Journaling Be A Part Of Your Internal Audit

Backtesting and journaling are important audit tools. A trader who cannot show how a strategy has behaved over time, which assets it works on, when it tends to fail, and whether actual execution matches the written method is not really operating a controlled process, they are simply going by gut feeling.

When your trading style is producing a lot of small, individual outcomes, it becomes especially difficult to evaluate based on memory and final bottom line. Our memories are not to be trusted. It is, for instance, not unusual for a trader to vividly remember dramatic wins, infuriating losses, and trades that “basically worked”, while forgetting dull mistakes, minor rule breaks, and the slow leak caused by mediocre setups taken in poor conditions. A spreadsheet does not have that problem, because it is unsentimental.

What to Measure

A usable journal for binary options needs more than entry and outcome. At minimum, it should capture the date, time, asset, direction, expiry, stake size, payout, brokerage company entity, setup type, higher timeframe bias, execution timeframe, and whether the trade followed the written plan.

The result should not only be a win or loss, but the exact result, and whether the trade was a good decision under the system regardless of outcome. That distinction sounds slightly fussy, but it is central. Traders who judge every decision by result alone end up training themselves to confuse luck with quality.

The point of measurement is not to produce beautiful dashboards for social media. It is to identify whether the supposed edge is concentrated somewhere real. Many retail traders do not have a strategy problem so much as a classification problem. Their good setups are mixed with too many low-quality ones, and without data they cannot tell which is which.

The Breakdown

Performance should be broken down by asset, time of day, session, day of week, setup category, and expiry band. Use the spreadsheet. Perhaps a trader’s EUR/USD continuation setups work reasonably well during the London-New York overlap but perform poorly in thin Asian hours. Perhaps five minute reversals are consistently weak while 15 minute retest setups are acceptable. Perhaps one broker shows noticeably worse realized results around major releases than another.

Spreadsheets, Ledgers, and Review Discipline

A spreadsheet is usually enough for most retail traders if it is structured properly. One sheet can hold raw trades. Another can summarize metrics by asset and timeframe. A third can track equity curve, drawdown, average payout, win rate, and expectancy by setup class. The goal is not complexity but traceability and pattern discovery.

A good ledger should also reconcile deposits, withdrawals, bonus credits if any were accepted, platform fees or conversion costs, and ending balances. This matters for two reasons:

- First, it helps the trader verify whether the platform’s history is complete and internally consistent.

- Second, it creates a foundation for tax reporting and dispute resolution if the platform later becomes less cooperative than it was during deposit month.

Review discipline matters as much as the spreadsheet itself. Weekly review is often enough for active traders, with a deeper monthly review to identify persistent behavioral leaks and actual performance characteristics. The review should ask plain questions:

- Which setups are positive?

- Which are negative?

- Which losses came from rule breaks?

- Which losses came from normal variance?

- Are certain expiries consistently mismatched to certain setup types?

- Is the trader drifting into overtrading after losses?

- Is the trader drifting into overtrading after strong winning runs?

Breaking Down Performance Data

Once your dataset spans a statistically relevant baseline, slice the metrics across narrow bands to isolate leaks:

| Analytical Slice | Target Assessment | Expected Action |

|---|---|---|

| Temporal Horizon | Performance compared across specific hours (London/NY overlap vs. illiquid Asian sessions). | Filter out low-liquidity blocks where broker payouts drop or spreads widen. |

| Expiration Bands | Success rates of 60-second scalps vs. 15-minute structural retests. | Eliminate expiration durations that suffer from excessive noise. |

| Broker Deviation | Win/loss ratios and realization times compared between different platform systems. | Identify if an offshore broker suffers from systematic execution delays. |

Weak Record-Keeping Can Produce Fake Confidence

Weak record-keeping can create fake confidence because it allows the trader to tell flattering stories to themselves. A few good wins feel like evidence of skill. A bad week is dismissed as unusual. A repeated mistake or the result of a broken rule is relabeled as bad luck. Over time, this creates a strange situation in which the trader feels more certain while knowing less.

If twenty trades are placed in a week, many traders can remember only the emotionally loud ones by the weekend. The spreadsheet, by contrast, will often show something less glamorous, such as one or two profitable setups done in accordance with the trading strategy and a long row of impulsive entries against the strategy rules.

This is why journaling should be treated as part of implementation, not as homework after the interesting part is over. It is how the trader verifies whether the strategy is valid outside their own narration. The market is already difficult enough. Inventing a false version of your own performance on top of that is not helpful.

Tax Obligations

Tax treatment is where many retail traders discover that “global binary trading” is not one tax category. Factors such as legal platform registry location, the country of trader residence, retail vs. professional, how active the trader is, and even the exact contract type can all change the result, depending on the circumstances. This is why local tax information pertaining to your specific situation is necessary.

When it comes to retail binary options, many retail traders live in countries where local brokers are not allowed to sell binary options to non-professional traders. So, traders sign up with foreign platforms, often ones located in lax jurisdictions far away. This introduces jurisdictional complexity, and it also means that you can not assume that reporting and record keeping provided by your broker will be enough to satisfy the demands of your own jurisdiction or be presented in a way that is streamlined with local requirements. Reporting standards vary from one jurisdiction to the next, and tax classification is rarely as simple as “profit is profit”.

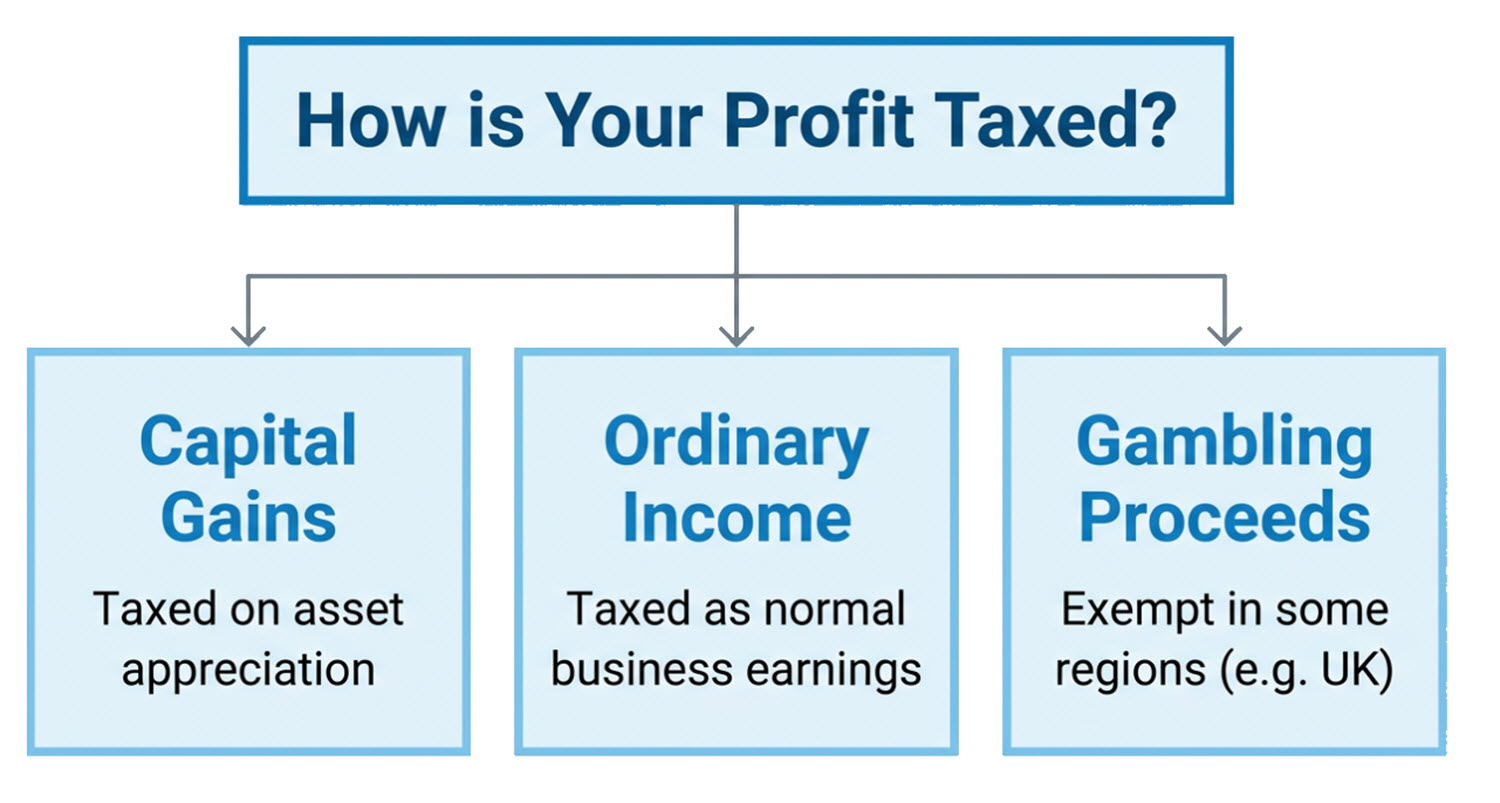

Depending on the country and your particular situation, gains from financial speculation may be treated as capital gains, ordinary income, business income, gambling or betting proceeds, or some awkward mixture that depends on several facts and circumstances. In the United States, for example, tax treatment can differ depending on whether the activity falls into securities trading rules, gambling income, or certain exchange-traded contract rules. In the UK, betting style gains are often outside ordinary tax treatment for the individual bettor, while other trading activities are not. Australia and Canada both distinguish between investing and carrying on a trading business, which changes tax treatment materially.

It is also important to remember that when brokers operate from lax jurisdictions with minimal broker oversight, they can allow themselves to be pretty lax about your records as well, and you might, for instance, run into a situation where you discover that your transaction history or win and loss statements are incomplete or contain errors. This is not a nice thing to find out in a situation when you really need to forward complete and correct documentation to your local tax authority as soon as possible to avoid complications and unnecessary costs.

Capital Gains, Trading Income, and Gambling Treatment

In many jurisdictions, the process of understanding your tax situation will start by figuring out what your binary options trading is classified as. Is it investing, trading, or maybe even gambling? Will your activity be considered a hobby that generates an income or is it a business?

Rules do not always line up neatly. Under one rule, you can be classified as a retail trader that does not reach the requirements to be re-categorized as a professional trader, while another rule in another part of the law book determines that your trading is sufficiently active to be taxed as business income and not a hobby.

Japan – An Example of How Binary Options Income Taxation Can Be Complex

Giving detailed legal tax advice for every country in the world from which our readers might be arriving at this page would not be possible. Instead, we will take a brief look at Japan, since that is a country where local brokers are allowed to sell retail binary options. By looking at how an individual binary options trader in Japan can be taxed in different ways depending on the exact circumstances, we will highlight some of the most important considerations. These considerations are not unique to Japan and they tend to impact taxation in many other jurisdictions around the world, although with great variations in the end result depending on the exact legal framework.

In Japan, retail binary options are legal but tightly regulated by the Financial Services Agency (FSA). Unlike the many jurisdictions that have banned brokers from selling retail binary options, Japan permits them through licensed financial firms operating under strict rules. Japanese regulation includes limits such as minimum expiration periods, standardized disclosures, and restrictions designed to reduce the resemblance to gambling.

The legal classification matters because binary options offered through licensed financial intermediaries are generally treated as financial derivative transactions rather than betting activity. As a result, profits are typically discussed within the framework of taxable miscellaneous or investment-related income rather than gambling exemptions. The practical point is that in Japan, binary options are treated according to the regulatory structure under which they are offered and the financial laws governing the provider.

In Japan, an important distinction is whether the trading activity should be treated as ordinary miscellaneous income (雑所得, zatsu shotoku) or as business income (事業所得, jigyō shotoku).

For retail binary options traded through regulated brokers, Japanese individuals are commonly treated as earning miscellaneous income rather than operating a formal trading business. But under Japanese tax principles, very active and organized trading can potentially rise to the level of a business.

How an individual binary options trader is classified matters a lot, because classification can impact things such as:

- destructibility of losses and expenses

- bookkeeping obligations

- loss carryforwards

- social insurance implications

- how income should be reported

For example, recognized business income may permit broader expense deductions than miscellaneous income.

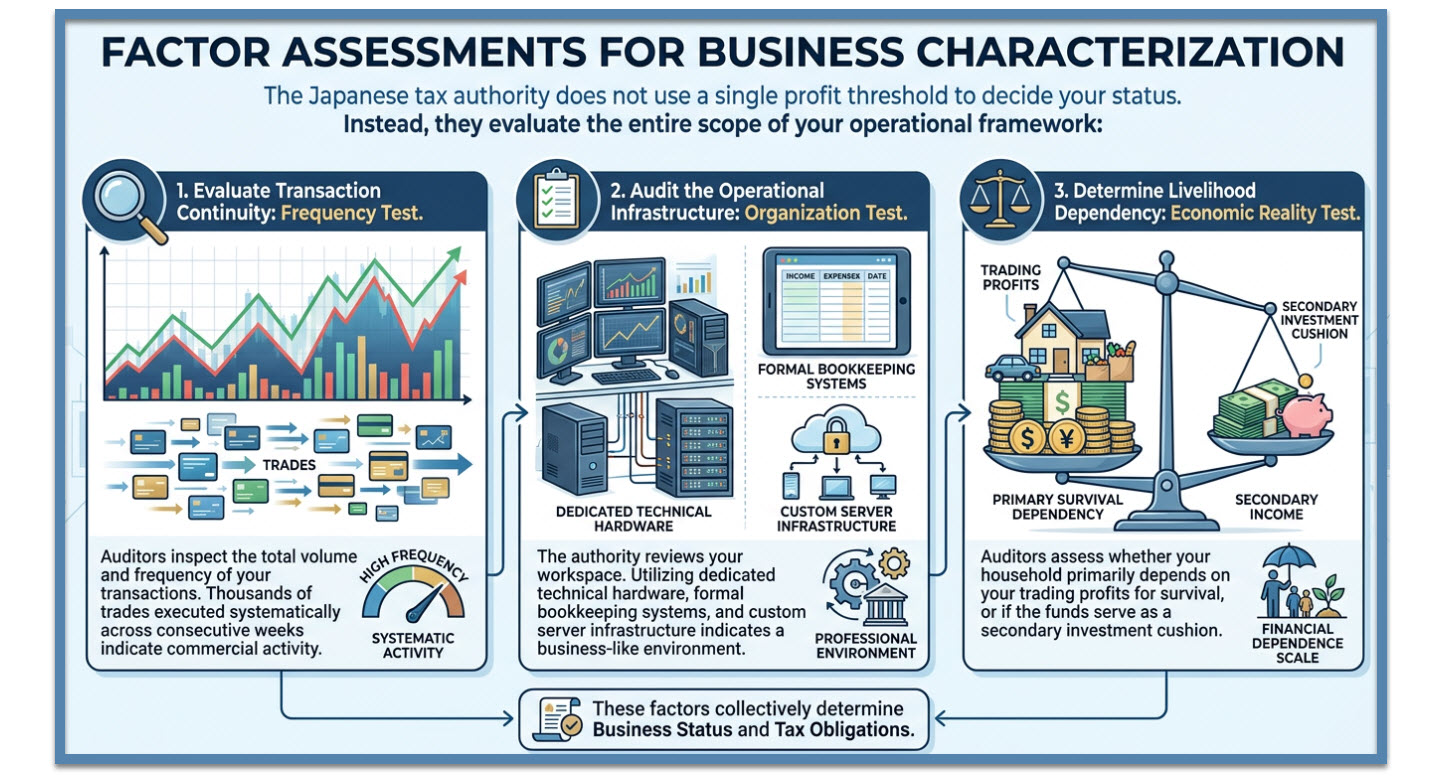

The Japanese tax authorities do not provide a single exact rule like “X trades per day means it is a business income” or “below Y amount of profit it is automatically a miscellaneous income”. Instead, classification depends on the overall factual picture, and this is something the Japanese system has in common with many other jurisdictions around the world. There will therefore always exist borderline cases where it can be difficult to know in advance exactly how the authority will treat the income.

Typical factors Japanese tax authorities and courts may consider include:

- scale and continuity of activity

- frequency of transactions

- degree of organization

- whether records and systems resemble a business

- dependence on the activity for livelihood

- profit motive

- if the person is operating the activity in a way that resembles a real ongoing business rather than occasional and casual personal trading

It should also be noted that for the individual, the overall assessment can include income from more types of trading than just binary options, and this can impact the final result. Japanese tax treatment of derivatives, FX, CFDs, cryptocurrency, and binary-style products can become technically complex because some products fall under separate self-assessment taxation regimes, some are exchange-traded, some are OTC, and different statutory categories can apply. The broker used, whether the product is domestically licensed, and what the legal structure of the contract itself looks like, can all be factored in.

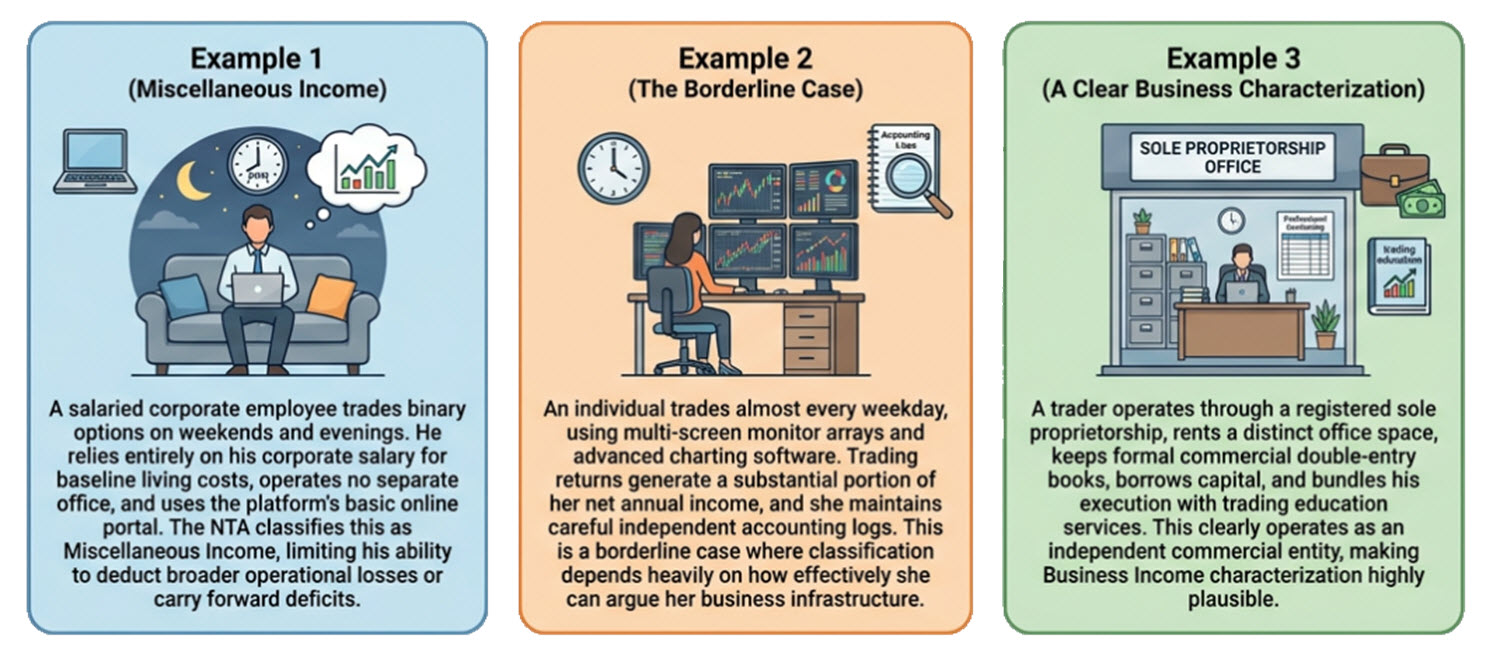

Example 1: This trader is likely to have their binary options trading treated as miscellaneous / non-business income

A salaried office worker is trading binary options on evenings and weekends. He places occasional trades during market events, earns irregular profits, and mainly relies on his salary income. He has no employees or office for the activity, and he keeps only basic necessary records.

Even if his profits are substantial in one year, this often resembles an investment or side activity rather than a standalone business.

In practice, this is frequently classified as miscellaneous income by the tax authority.

Example 2: Borderline case

This is a person who trades almost every weekday and earns a substantial part of her total annual income from binary options. She uses several monitors and dedicated advanced software, spends a lot of time studying markets, and consistently trades for short-term profit. She maintains detailed accounting records.

This begins to look more business-like, and the Japanese tax authorities could potentially view this as business income depending on the overall facts and economic reality.

Example 3: This trader is likely to have their binary options trading treated as business income

This trader operates through a registered sole proprietorship, has a dedicated office, and maintains formal bookkeeping. He conducts thousands of transactions annually, borrows capital for trading, and depends primarily on trading profits for livelihood. He also markets and sells trading-related services and education.

This more strongly resembles an independent commercial activity rather than passive investing or casual speculation, and business income characterization becomes very plausible.

Don’t Trust Vague Broker Promises

As you can see, binary options trading can be classified in different ways by the relevant tax authority or authorities, depending on applicable laws and the exact circumstances. In some jurisdictions, binary options profits may be treated more like gambling proceeds for the individual and may sit outside ordinary capital gains rules. In others, repeated short-term trading activity may be classified as hobby income or business income. In others still, the underlying instrument that you are speculating on using binary options may impact whether the gain is reported as ordinary income or under a special derivatives regime. That means the same economic activity can produce very different tax outcomes depending on where the trader lives and what exact legal form the product and the trading activity take.

Because of all this, traders should be extremely suspicious when trading platforms and adverts happily proclaim how trading with this particular broker will provide you with tax-free or tax-advantaged income. They don’t know your exact tax situation and they only make these wild and sweeping claims when they know they won’t be held accountable for the “advice”. The tax authority in your country will not grant you an exception from national tax law because you were promised tax-free trading by a foreign broker.

A sensible approach is, therefore, to do your own due diligence. Ideally, obtain the information in advance and adapt your trading accordingly to get the best possible outcome. Do not wait until the filing deadline is close and you have put a year of trading behind you, not knowing how your income is likely to be classified by the tax authority. This means identifying the points that the relevant tax authority or authorities will use to decide whether the activity is a hobby that might generate some income or if it is investing or trading in a business form. You also need to know if local reporting rules even apply to your income from a foreign platform.

Platform Records May Not Be Enough For Full Tax Compliance

Most brokers provide transaction history, but that does not mean they provide adequate tax records that will be accepted by the relevant tax authorities. Foreign platforms may, for instance, use server time that does not match the trader’s tax residence, they may not show clear legal entity names on all statements, and currency conversions may be implicit rather than stated. Simply showing deposits and withdrawals will not be enough if the authority wants to see your trade history. Bonus adjustments, rebates, and manual corrections can muddy the ledger further.

For tax purposes, traders usually need more than a brief record of deposits and withdrawals. They need account statements, trade confirmations, and a self-maintained ledger that reconciles the numbers. If a tax authority later asks how the reported figure was derived, “the platform balance looked about right” will not be an ideal answer. This is particularly important where tax treatment depends on whether the activity was carried on like a business or not.

Transitioning Your Trading From Being Entertainment To An Activity Marked by Professionalism

When we discuss this, it is important to keep three different things separate:

- Going through the process of being classified as a professional trader (not retail traders) in the eyes of the relevant consumer protection laws. Depending on the jurisdiction, being classified as a professional trader can, for instance, make it legal for the broker to give you access to higher leverage, a trading account without Negative Balance Protection, and certain non-retail financial products. In many jurisdictions, brokers are not allowed to sell binary options to traders who are not classified as professional traders in this sense, so the distinction matters a lot.

- Having your trading activity classified as a business or business-like trading by the tax authority. This has to do with how your income will be taxed, which deductions you can take, and so on. In many jurisdictions, it is possible to have your trading activity classified as business or business-like, even if you are using a retail account and have not gone through the process of being classified as a professional trader under relevant consumer protection laws.

- Getting into the mindset of viewing your own trading as a serious activity marked by professionalism rather than a fun little hobby where the aim is to learn a bit more about markets, or an exciting activity you do chiefly for entertainment purposes. This point is focused on your own mindset, decision-making process, and administration.

Of course, all three points outlined here are connected to each other in various ways, but they are not identical. It is possible to be classified as a retail trader under consumer protection laws and as a hobby trader by the tax authority, and still approach your trading with a high degree of professionalism. While going through this mindset change, it is important not to fall into the trap of equating professionalism with grand language, overtrading, and oversized positions. On the contrary, it will involve even stricter risk management routines, more well-motivated decisions regarding when you open a position and how much to stake, and a lot of detailed administration. It will be less about posting impressive screenshots online and more about maintaining proper records, controls, and documented procedures, and always having the ability to explain what was done, where, when, and why.

Audit Ledgers and Documentation Standards

An audit ledger is simply a record set that another person could follow without needing your memory to fill in the gaps. For a binary trader, that involves preserving trade logs, payout rates, session notes, monthly statements, deposit and withdrawal evidence, identity documents used with the broker, and a journal showing how setups were classified. It also means noting which legal entity actually held the account, especially where brokers operate multiple entities across jurisdictions.

An audit ledger helps bring operational clarity, and it is important for both your internal process and for your interactions with others, e.g. your broker, the financial authority, the tax authority, and other relevant entities. If a withdrawal dispute appears, if a bank asks questions about incoming funds, or if an accountant needs to reconstruct the year, the ledger should make that process possible without detective work. Traders who rely only on the platform portal to provide them with all the documentation tend to discover the weakness of that approach when push actually comes to shove.

You can not trust the platform to have all the necessary information logged, with sufficient detail. You can not trust the platform to provide you with uninterrupted access to this information. You can not trust the platform to make no manual changes to historic information. This is especially true for brokers based in lax jurisdictions with very limited broker oversight. There are also issues to consider concerning company ownership changes, technical problems, hacker attacks, and more. If information is important, you need to keep relevant copies with you, and not only on the broker’s server.

For your own internal process, good documentation standards can help improve strategy review. If the trader can trace not only trade outcomes but also which version of the strategy was in use, what filters were applied, and what broker conditions existed at the time, then performance analysis becomes much more reliable.

Legal Due Diligence on Brokers, Entities, and Payment Trails

A process marked by professionalism also means understanding who the trader is actually dealing with. The brand name on the homepage is not the most important legal fact. You need to know and document your actual counterpart. It matters a lot if your legal counterpart is based in your own country, in a country where it is supervised by a strict financial authority, or in a lax offshore paradise.

Before you even sign up to trade binary options, you should make sure you know who your legal counterpart will be, where that entity is incorporated, which law governs the contract, the name of the relevant financial authority and its reputation for trader protection, where your account money will be stored, and if mandatory client asset segregation applies.

Legal due diligence also includes checking whether applicable laws treat your access to binary options differently from the broker’s own marketing claims. A trader does not need a law degree to recognize a simple principle: platform claims are not necessarily the same as what applicable law actually permits or how applicable tax law will classify your gains.

If funds move through unusual third-party processors or crypto rails with weak record-keeping, reconstruction becomes harder later. Instead of your deposit going directly to the broker through a mainstream bank or card network, it may pass through obscure payment companies, shell businesses, offshore e-wallets, or seemingly unrelated merchant accounts. You are funding your trading account, but your statement shows that you have sent money to an obscure marketing company based in Farawayistan. If governmental authorities (e.g. tax authority and financial authority) later try to reconstruct and understand your activities and transactions, it can be difficult for you to prove where your money actually went and whom you have been receiving money from and why.

Using cryptocurrency comes with its own set of possible issues down the line, including unclear wallet ownership, limited customer identification, incomplete transaction records, and brokers deliberately engaging in tumbling/mixing to obscure the trail.

Having A Professional Mindset

The hobbyist mindset usually treats trading as a stream of exciting market moments. The professional process mindset treats it as an activity with inputs, outputs, records, and obligations. This means building a routine where every trade can be traced, every monthly result can be reconciled, and every claimed edge can be examined in data rather than in memory. It means not accepting a broker bonus without understanding turnover terms and accounting consequences. It means not assuming tax treatment based on broker claims in flashy adverts. It means preserving evidence while everything is functioning normally because evidence is always easier to collect before trouble starts.

None of this guarantees profit, but it reduces avoidable confusion, and it places you in a better position for your interactions with other entities. For many retail traders, confusion outside the market causes as much damage as confusion inside it. Funds become hard to document, results are hard to analyze properly, and a decent trading year becomes administratively messy because the back office was treated like an optional extra. A professional mindset is largely about being traceable, reviewable, and well-prepared.