Are Prediction Markets The New Insider Trading?

In January 2026, a US Army Master Sergeant named Gannon Ken Van Dyke allegedly walked away with $400,000 from a prediction market. He’d bet on the capture of Venezuelan President Nicolás Maduro. He knew it was coming because he helped plan it. That’s the story that broke the dam. Lesser-known stories are also cropping up, including the Google software engineer who allegedly made around $1.2 million by using internal data to make a batch of trades on Polymarket.

Prediction markets had been growing quickly. Monthly volume on Kalshi and Polymarket reached about $24 billion in April 2026, up from less than $5 billion just seven months before, according to Pew Research. Bernstein now expects prediction markets will grow to $1 trillion by 2030.

For a while, the industry avoided regulatory trouble and ignored concerns about insider trading. Van Dyke’s indictment changed that. The DOJ and CFTC acted within days of each other, sending a clear message: prediction markets are not exempt. Existing fraud laws already apply.

This article is primarily for binary options traders who follow prediction markets and want to understand the legal boundaries. The products are similar, with the same yes/no payout structure but different underlying events. However, the insider risk is different in ways that matter under the law.

Recommended Prediction Markets Platforms

| Broker | Min Deposit | Expiry Times | ||

|---|---|---|---|---|

|

Crypto.com | Varies by payment method | 5 minutes to event cutoffs, can be hours, days and longer depending on contract | » Visit |

Crypto.com Prediction Markets

Crypto.com is a great choice for traders wanting to deal prediction markets on an intuitive app. Regulated by the CFTC, you can place simple yes/no bets on a wide range of events, from presidential elections to movements in the S&P 500, with contracts traded like shares. It doesn’t offer some of the advanced analysis tools and features of prediction markets platforms like IBKR’s ForecastTrader, but for mobile-first retail investors, Crypto.com is a user-friendly fit.

Visit

Prediction Markets Vs. Binary Options: Same Structure, Different Exposure

If you have traded binary options, prediction market event contracts will seem familiar. You buy a position on a yes-or-no outcome. If you are right, you get $1.00. If not, you get $0.00. The price shows the implied probability. That’s the basic idea.

The real differences are below the surface.

| Feature | Binary Options | Prediction Market Event Contracts |

|---|---|---|

| Counterparty | Typically a broker/dealer | Other market participants |

| Underlying event | Usually a price level, such as gold above $1,900 | A real-world outcome, such as Maduro out of power by January 31 |

| Pricing mechanism | Set by the platform | Determined by continuous market trading |

| Primary regulator | Varies, unregulated in some jurisdictions | CFTC, as commodity derivatives or swaps |

| Exchange structure | OTC or exchange-traded | Designated Contract Market |

| Insider risk profile | Lower—anchored to price data that is broadly public | Higher—anchored to real-world events where insiders exist |

The Van Dyke example is the one now leading to federal indictments. If your underlying event is a price level, only a small group – mainly market participants and corporate insiders – might have key private information. But if the event is something like “Will the US invade Venezuela by January 31?”, the group grows to include anyone with a security clearance, inside sources, or close contact with top officials.

Prediction markets do not just have more potential insiders than binary options; they face a different kind of insider problem altogether.

How The Law Works

Many people are unsure if this is technically illegal. The term “insider trading” does not appear in the relevant law. Because of this, some participants – and some confident voices on crypto X – think the rules do not apply.

They do.

Prediction market event contracts are considered commodity derivatives or swaps in the US. This means the CFTC, not the SEC, oversees them. The main enforcement tool is Section 6(c)(1) of the Commodity Exchange Act, along with CFTC Regulation 180.1, which bans any “manipulative or deceptive scheme” involving commodity contracts.

Regulation 180.1 was designed to match SEC Rule 10b-5, the main insider trading rule for securities. In March 2026, CFTC Enforcement Director David Miller explained at NYU Law School that both rules are part of the Dodd-Frank Act’s effort to give the CFTC greater power to address fraud and insider trading in commodity markets.

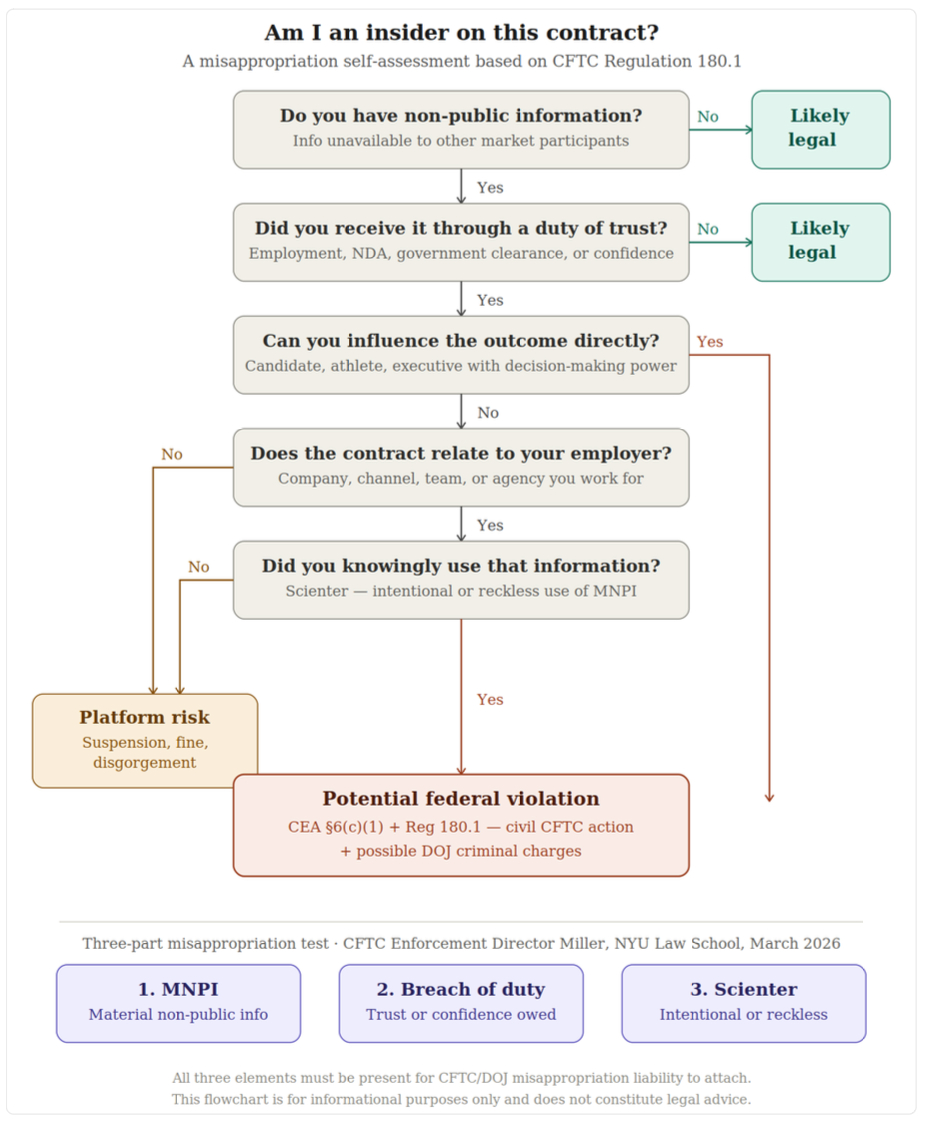

The legal theory used here is called misappropriation. It doesn’t require you to be a corporate insider in the traditional sense. It attaches liability when:

- You possess material non-public information, or MNPI.

- You trade on it in breach of a duty of trust owed to whoever gave it to you.

- You do so knowingly or recklessly.

The third element, intent, also called scienter, is important. Recklessness is enough to meet this standard. You do not have to think, “This is probably illegal.” If you knew the information was confidential and traded on it anyway, that likely counts.

Not sure whether a specific trade you’re considering crosses any of these lines? The flowchart below works through the test.

Follow this flowchart to understand whether you may qualify as an insider trader on an event contract

There’s also a separate, more stringent provision for government employees. The STOCK Act and Section 4c(a)(4) of the CEA prohibit federal employees from using non-public government information to trade in commodity markets. That’s the provision Van Dyke ran directly into.

What’s Legal & What Isn’t

The CFTC’s distinction, which courts have supported, is not about having more information than others. Derivatives markets have always allowed trading on better information. What is banned is trading on information you obtained by breaking a duty of confidence.

| Legal | Potentially Criminal |

|---|---|

| Deep research into public data | Using classified intelligence |

| Better political analysis than your counterparty | Breaching an NDA to front-run an announcement |

| Aggregating public signals faster than others | Betting on an outcome you’re personally shaping |

| A well-reasoned opinion | Trading on something told to you in confidence |

The problem is not having more information. The issue is how you got it.

Platforms are also taking steps to try and prevent insider trading. For example, some users on Kalshi will have to declare where they work.

Three Cases, Three Kinds Of Insider

Case #1: The Soldier

Van Dyke’s case is the one that opened the door to criminal law. He was a Master Sergeant with Joint Special Operations Command, stationed at Fort Bragg. He was a communications specialist and was involved for roughly a month in planning Operation Absolute Resolve, the mission to capture Maduro.

Starting December 26, 2025, he placed $33,034 across 13 Polymarket bets, all pointing “Yes” on Venezuela-related contracts with a January 31 deadline. Maduro was seized in the predawn hours of January 3. Van Dyke cleared roughly $400,000.

He’d signed NDAs. He then apparently tried to delete his Polymarket account. Prosecutors say he falsely claimed he’d lost access to the associated email address. In April 2026, the DOJ unsealed charges for unlawful use of confidential government information, theft of non-public government information, commodities fraud, wire fraud, and unlawful monetary transactions. Five counts. The CFTC filed a parallel civil complaint the same week under Regulation 180.1.

US Attorney Jay Clayton put it plainly: “Prediction markets are not a haven for using misappropriated confidential or classified information for personal gain.”

This was the first time the DOJ and CFTC brought charges together for prediction market trading. It likely will not be the last.

Case #2: The Candidates

The day before Van Dyke’s indictment, Kalshi made its own announcement: three congressional candidates had been fined and suspended for five years for betting on their own races.

Mark Moran, running for the Virginia Senate, had placed bets on himself under a “Who will run for public office this year?” contract before publicly announcing his candidacy. Kalshi’s filing described him as “a direct decision maker for this contract” who “had direct influence on the outcome.” He was fined $6,229.30 plus disgorgement. Ezekiel Enriquez and Matt Klein each wagered on their own primaries and paid smaller fines – $784 and $539, respectively.

Klein’s case is legally interesting. He told the press he bet $50 on himself after friends told him about the market, and he was curious. He called it a mistake. Kalshi still banned him for five years. The size of the trade did not matter. What mattered was that he had non-public information about his own plans. Whether he would stay in the race, drop out, or change strategy was not known to the other side of his trade.

This shows how insider risk can affect prediction markets and make them unusual. You do not need access to military intelligence. Just running for office is enough.

Case #3: The Video Editor

Two months before any of the above, in February 2026, Kalshi quietly suspended a MrBeast video editor named Artem Kaptur.

His account had been flagged by Kalshi’s surveillance team for what the company described as “statistically extreme” win rates on markets tied to MrBeast content. These included bets on specific words the creator would say in unreleased videos, streaming milestones, and video performance. As an editor, Kaptur had seen the content before it went public. He was ordered to disgorge $5,397.58 in profits, pay a $15,000 penalty, and serve a two-year suspension.

The CFTC cited this case in its February 2026 enforcement advisory as an illustration of the exact conduct Regulation 180.1 covers: the misappropriation of confidential information in breach of a duty of trust owed to an employer. It also noted, pointedly, that while Kalshi handled the matter internally, the Commission “has full authority to police illegal trading practices occurring on any DCM.” In other words, the platform fining someone doesn’t close the book.

The Kaptur case is important beyond MrBeast because prediction markets now include contracts on film release dates, sports team decisions, earnings reports, government policy actions, and box office results. Each of these areas has its own insiders, such as studio employees, team staff, or government contractors. Many of them are not thinking about CFTC Regulation 180.1, but some probably should.

Where Regulation Is Heading

The Van Dyke indictment was a criminal case using current law. Regulators are working on a new framework – rules that will guide the industry going forward, rather than only reacting after problems occur.

The CFTC’s advisory reminds platforms and users that Regulation 180.1 applies to prediction markets and that the Commission will investigate and prosecute violations. This was not a new rule, but a warning. Formal rulemaking began in March 2026, when the CFTC published an Advanced Notice of Proposed Rulemaking, or ANPRM, seeking public comments on a new framework. The comment period ended on April 30.

Meanwhile, the DOJ and CFTC jointly sued Illinois, Connecticut, and Arizona in April 2026, asserting that federal CFTC jurisdiction over event contracts is exclusive and pre-empts state-level attempts to restrict the platforms. That case will determine whether prediction markets are primarily a federal product or subject to a patchwork of state rules. Use our US state-wide checker to see the legal status of prediction markets.

On the rulemaking side, expect a formal Notice of Proposed Rulemaking in 2026 or early 2027, with final rules and compliance deadlines likely in 2027–2028. Crowell & Moring described it as “likely to be a multi-year rulemaking process.”

Those final rules will probably require mandatory identification of restricted participants, such as politicians, employees of relevant companies, and government workers; pre-trade screening systems; real-time surveillance with escalation to the CFTC; and clearer tests for which event contracts can be listed at all.

To give some context on timing, the CFTC’s first insider trading case under Regulation 180.1 in a traditional commodity market happened years after the Dodd-Frank rules were passed. Enforcement usually happens before formal rulemaking, which is what is happening now.

Sidebar: UK & EU Exposure

Most of the enforcement activity above is US-based, but the insider question doesn’t stop at the border.

In the UK, neither Polymarket nor Kalshi is authorised by the FCA. The UK Market Abuse Regulation, or MAR, which derives from EU law, became the retained domestic regime at the end of the Brexit transition, effectively from January 1, 2021, bans insider dealing and market manipulation involving financial instruments. If a prediction market event contract is treated as a financial instrument under UK law, which remains unclear, trading on material non-public information could breach UK MAR rules. Criminal penalties can be up to 10 years.

The FCA’s 2019 ban on retail binary options also likely applies to contracts that settle at $1.00 or $0.00, which matches the structure of Polymarket contracts. No enforcement has happened yet under this rule, but regulators could use it.

In Europe, the situation is more complicated. As of early 2026, France, Belgium, Poland, Portugal, Hungary, Romania, and Ukraine had banned or restricted Polymarket. Germany, Spain, Denmark, and Greece still allowed it. In February 2026, the Netherlands Gambling Authority, the Kansspelautoriteit, threatened fines of €420,000 per week.

There is no single EU framework. Platforms fall under both gambling and derivatives rules, with no single regulator in charge. Under EU MAR and MiFID II, trading on non-public information in a contract treated as a financial instrument can be a crime. However, the classification of these contracts varies by country.

Robinhood is reportedly in active discussions with the FCA and EU regulators about launching prediction markets internationally. When that happens, the classification question will be forced, which matters for anyone trading now under the assumption that an unregulated offshore platform creates legal distance.

5 Things To Check Before Your Next Prediction Trade

Rules are still being developed, but enforcement is already happening.

- Check your employment contract. Confidentiality clauses still apply, even if you are trading an event contract instead of a stock. If your job gives you non-public information about an employer, client, or government programme with a live prediction market, and you trade on it, you are likely breaking both your contract and Regulation 180.1.

- Determine whether you are a restricted person for a specific contract. It is not just politicians and soldiers. Athletes betting on their own leagues, studio employees trading on unreleased film dates, and sports agents with injury information can also be restricted. The group of people with a duty of confidence who could profit from trading is large, and platforms are still working on systems to detect this automatically.

- Remember that tipping also counts. You do not have to place the bet yourself. The misappropriation rule also applies if you give the information to someone else who then trades on it. Both the original insider and the person who receives the tip can be held responsible.

- Platform fines are not the maximum penalty. Kalshi banned Kaptur internally, but the CFTC later used his case as an example and made it clear that it could have taken its own action. A platform suspension and a $20,000 fine are just the minimum possible consequences, not the most you could face.

- Keep records of your research. If a trade is successful and gets attention, you may need to explain how you obtained your information. Analysis of public data, written reasoning, and timestamped research notes can help show that your advantage came from your own work, not from inside information.

The Broader Point

Prediction markets can serve a real public purpose by bringing together scattered information into prices and giving researchers and journalists a real-time sense of what informed people believe. This only works if participants trade based on analysis, not by breaking confidences. If prices start to reflect insider leaks rather than honest beliefs, the market stops being a useful information tool and becomes a way for people with secrets to profit.

This is why insider trading rules should apply to prediction markets, not just stocks. The main issue is not fairness, though that matters too. The real question is whether the product still works once it is affected by insider trading.

The Van Dyke case, the Kalshi candidate bans, and the MrBeast editor are not rare exceptions that just happened to get noticed. They show a bigger problem that grows as the market expands. More contracts create more types of insiders. More trading volume increases the temptation to use non-public information. Regulators are struggling to keep up, much like what happened with binary options in the early 2010s.

The difference now is that the CFTC is acting more quickly, the DOJ is already involved, and the platforms are cooperating instead of resisting. The big question is whether this will be enough to build trust before another major case appears.