Are Prediction Markets Halal or Haram?

Polymarket handled more than $3.6 billion just on the 2024 US presidential election. In September 2024, Kalshi won a federal court case allowing it to offer political event contracts in the US, despite objections from the CFTC. Some of this volume, along with growing interest, comes from the UAE, Saudi Arabia, and Indonesia, where Islamic finance is the standard, not a specialty. This naturally leads to the question:

Are prediction markets allowed or not for Muslim traders?

We’ve evaluated both sides of the debate, read a huge range of religious guidance on the matter, and while many lean on the haram side, there’s not always a clear answer. This isn’t due to slow scholarship, but because prediction markets sit at a difficult intersection in Islamic commercial law, where several important principles and opposing views meet. What follows is not a fatwa, but rather the main points you can discuss with a scholar who understands these platforms.

Disclaimer: This content does not constitute formal Islamic legal rulings (fatwas), financial advice, or religious counsel. Always consult a qualified Shariah scholar regarding your personal financial and investment choices.

Before we begin, it’s important to know that the answer depends on whom you ask. Islamic law is not a single school of thought. The Hanafi madhab, common in Pakistan, Turkey, and much of South Asia, applies strict rules about Gharar in financial contracts.

The Maliki and Hanbali schools carry greater influence in Saudi Arabia and the Gulf and place greater weight on Maslahah, or public interest, when judging new financial products. So, a Hanafi scholar in Karachi and a Hanbali scholar in Riyadh might look at the same Kalshi contract and come to different, but reasonable, conclusions.

This isn’t an inconsistency; it’s a centuries-old legal tradition meeting a very new financial product.

What You’re Actually Buying

If you’ve traded binary options, the mechanics here will feel familiar. Almost identical, actually.

On Polymarket or Kalshi, you buy a Yes/No token linked to a real-world event. If the event goes your way, the token pays $1.00. If not, it pays $0.00. The price changes between these points as new information and crowd opinions come in.

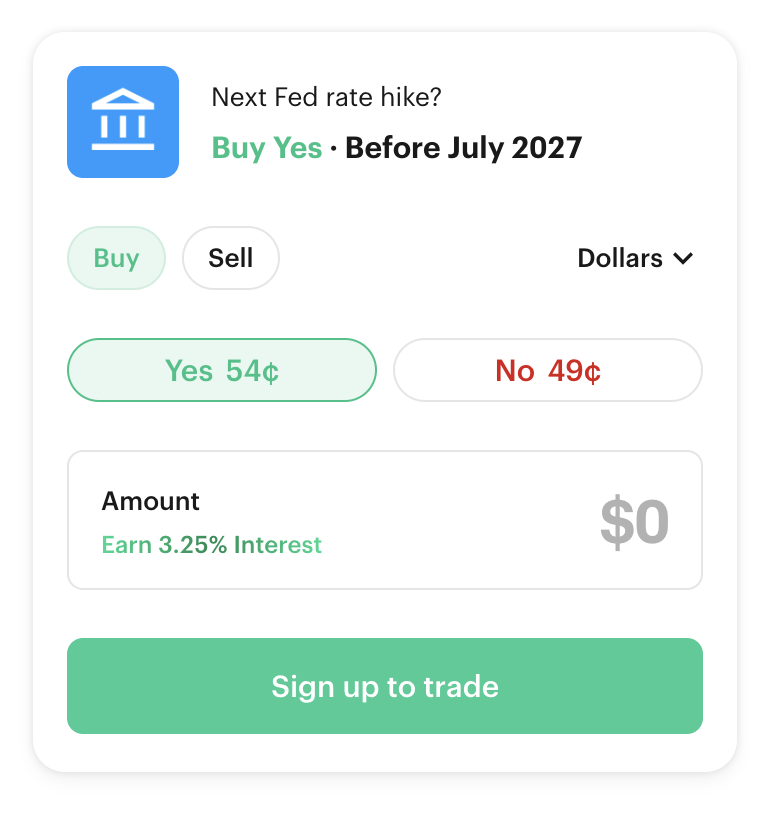

Kalshi offered a contract: “Next Fed rate hike — Before July 2027?” The Yes token traded at $0.54, and the No at $0.49. This suggests the market sees about a 54% chance that the Fed will raise rates before July 2027, even though most analysts still expect a rate cut.

If you buy 100 Yes tokens for $54 and the Fed raises rates before July 2027, you get $100. If there is no hike, you lose your $54.

Also, Kalshi shows “Earn 3.25% Interest” on idle funds in your account. This is important for Muslim traders to consider, and we’ll examine it further later.

Kalshi pays account interest – a largely haram practice due to the riba

Here’s how the contract sits against a binary options trade on the same underlying event:

| Feature | Binary Options Trade | Prediction Market (Kalshi) |

|---|---|---|

| What you’re trading | EUR/USD must hit a price level by expiry | Whether the Fed raises rates before July 2027 |

| Stake | $100 | $100, approximately 185 Yes tokens at $0.54 |

| Win condition | EUR/USD above 1.0850 at 3pm | Fed announces a rate hike before July 2027 |

| Win payout | $180, an 80% fixed return | Approximately $185, based on tokens × $1.00 |

| Loss | −$100 | −$100 |

| Exit early? | Rarely, at the broker’s discretion | Yes – sell at market price anytime |

| Price driver | Broker spread and volatility | Crowd wisdom and macro data |

And for context against other instruments:

| Asset Type | What You Own | Source of Profit or Loss |

|---|---|---|

| Traditional Stock | Equity in a real business | Growth, dividends, and market demand |

| Sports Bet | Wager against a bookmaker | Zero-sum transfer based on a game outcome |

| Binary Options | Time-limited price contract | Price movement at expiry |

| Prediction Market Token | Event-outcome contract | Crowd shifts and event verification |

The main difference from binary options is that prediction markets settle based on real-world events that can be independently verified, such as Fed minutes, official election results, or published GDP data, rather than a specific price at a certain time. This difference is important in Shariah analysis.

Why Most Scholars Say Prediction Markets Are Haram

Three concepts drive the case for prohibition, and each has teeth.

Maysir

Maysir is the Arabic term for gambling. What distinguishes it from legitimate commerce isn’t really about chance versus certainty – plenty of halal businesses involve uncertainty. It’s about whether wealth is transferred purely on the basis of an outcome, with nothing productive happening in between.

Zoya Finance, which screens individual stocks and funds for Shariah compliance, reviewed election contracts on Kalshi and Polymarket and concluded that the instruments “offer no ownership stake, equity, or claim on any underlying asset and exist solely to facilitate bets on future events.” Their ruling: Maysir, regardless of how much research the trader did beforehand.

It’s difficult to dispute this at a structural level. The Kalshi Fed rate-hike contract, with Yes at $0.54 and No at $0.49, shows how it works. If the Fed hikes and you have Yes tokens, money moves from No holders to you. Nothing is produced or delivered; it’s just a transfer.

There is also the “Earn 3.25% Interest” feature shown on the Kalshi trading screen. Any idle funds in your account automatically earn interest. This is Riba, and it is clearly visible on the platform before you even make a trade.

This is more than a small detail because there is no way to opt out. Kalshi’s help documentation says the 3.25% APY applies to all eligible accounts. It is added daily to both your cash balance and open positions and paid monthly. You cannot turn it off.

For Muslim traders, this means the Riba issue is not just in the contracts, but in the account itself. You cannot keep funds on Kalshi without earning interest, even if you never trade.

Polymarket, which uses USDC on the Polygon blockchain, does not have this feature, but it has its own issues with the UMA arbitration model, which we will discuss soon.

Gharar

Classical scholars prohibited contracts in which the outcome is sufficiently uncertain that one party is likely to be exploited. The test isn’t “does any uncertainty exist?” – every commercial transaction has some – it’s whether the uncertainty is the substance of the contract.

Prediction-market contracts often are exactly that.

“Will Apple release an AI hardware device before Q4 2027?” depends entirely on an undisclosed internal decision at Apple. There’s no deliverable. No price for a known good.

AAOIFI Shariah Standard No. 31 sets out the circumstances in which gharar, or contractual uncertainty, becomes sufficiently serious to invalidate a financial transaction. Prediction-market contracts may raise these concerns because the parties’ entitlement to payment depends entirely on an uncertain future event. However, AAOIFI has not, in the sources reviewed, issued a specific classification of Polymarket or Kalshi contracts, so applying the standard to these platforms is not definitive.

The Gharar issue is most evident in Polymarket’s dispute history. The Israel-Hezbollah ceasefire contract from late 2024 ran to several paragraphs of resolution criteria, defining what counted as an “official” announcement, which parties needed to confirm it, and whether a humanitarian pause qualified.

A trader, Garrick Wilhelm, bet on it and ended up in UMA arbitration when the outcome was contested. His money was decided by anonymous token holders – some of whom, a Wall Street Journal investigation later found, held positions in the same markets they were voting on.

Over 60% of active UMA voters were linked to Polymarket accounts. That’s not a regulatory edge case. That’s the Gharar problem made concrete.

Qabd

Qabd means possession. Islamic commercial law requires that a valid transaction involve a genuine transfer of something with productive utility.

A Yes token on “Will Bitcoin exceed $150,000 in 2027?” gives you no Bitcoin, no claim on any asset, and no service. You own a speculative contract.

Mufti Faraz Adam, one of the most cited scholars in Islamic fintech and a regular contributor to IFG’s Fatwa Forum, has argued consistently that instruments lacking genuine Qabd can’t meet the threshold for valid Islamic commercial exchange.

The Arguments For Prediction Markets Being Halal

These arguments are not as strong as those for prohibition, but they are still worth considering.

Maslahah

Maslahah means public interest. Prediction markets produce something genuinely useful: accurate probability estimates for future events, derived from people putting real money at stake.

On election night 2024, Polymarket repriced faster than any network’s decision desk, reflecting incoming results. Its final pre-election odds – Trump 54.8% and Harris 45.1%, with $3.7 billion in backing – were directionally correct when RealClearPolitics and FiveThirtyEight were calling the race essentially even.

Kalshi’s economic contracts, covering inflation and Fed decisions, are actively cited by researchers and decision-makers.

Islamic Finance Guru, whose February 2026 review of Polymarket and Kalshi landed firmly on the haram side, still framed the alternative productively: rather than betting on an outcome, “look for the actual consequences of that outcome and invest there.”

That framing doesn’t dismiss the analytical value – it redirects it.

The Hedging Case

Islamic law permits Salam contracts, or forward agreements, in which full payment is made up front for the delivery of goods at a later date. The explicit purpose is to let producers manage real economic risk. So, what happens when you apply that logic here?

Say you’re a UK importer. You have $200,000 in US-manufactured goods on order. Kalshi is running “Will the US impose 25%+ tariffs on manufacturing imports by December 2027?” at $0.40.

Your exposure if tariffs land is $50,000. To hedge that fully, you buy 50,000 Yes tokens for $20,000. If tariffs hit, you receive $50,000, mostly covering the additional cost. If they don’t, you lose your $20,000 premium but have no tariff exposure.

That’s a hedge ratio of 40 cents per dollar of exposure – the contract price itself.

Some may argue risk-transfer instruments in which the trader holds genuine, documented underlying exposure can be permissible.

The same instrument used with no underlying position – purely to speculate on the tariff outcome – is Mughalabat: financial wagering. It is the same contract but a different ruling, depending entirely on context.

Skill Versus Chance

Some discussions of Maysir distinguish activities dominated by chance from legitimate commercial activity involving knowledge, effort and informed risk-taking.

Predicting Fed rate decisions requires macroeconomic research. It’s not a coin flip. Whether that distinction is enough to clear the Maysir bar is unresolved, but it’s a question serious scholars are taking seriously, not dismissing.

The Shariah Scorecard

| Feature | Shariah Risk Factor | Permissibility Argument |

|---|---|---|

| Binary $1/$0 payout | High Maysir risk – zero-sum transfer | Can function as a hedge against real exposure |

| Outcome dependency | High Gharar – unknown future event | Research-driven, not random |

| No underlying asset | Qabd unfulfilled | Generates accurate public data through Maslahah |

| Crowd price discovery | Neutral | Can outperform conventional forecasting |

What to Do Instead – and The Account Question

If you conclude prediction markets are off-limits, the practical question is where to redirect the identical analytical energy.

I’d approach it this way. Take a live prediction-market thesis say, the AI infrastructure build-out. Instead of buying a Yes token on “Will OpenAI release GPT-7 before December 2027?”, I’d look at what grows regardless of which specific product ships and when.

The chipmakers. The hyperscalers. The companies that supply the physical infrastructure. That’s where the macro bet actually lives. IFG’s framing holds: find the practical consequences and invest there.

On the fund side, the SP Funds S&P 500 Sharia Industry Exclusions ETF (SPUS) or the Wahed FTSE USA Shariah ETF (HLAL) both give you that exposure.

Here’s what screening removes from a standard index:

| Screen | What Gets Cut | Why |

|---|---|---|

| Riba | Banks, conventional insurers, and most financial services | Revenue from interest is prohibited |

| Debt threshold | Companies with debt above approximately 33% of market capitalisation | Excessive leverage is a Shariah concern |

| Haram industries | Alcohol, tobacco, weapons, and adult entertainment | Direct prohibition |

| Impure revenue | Companies receiving more than 5% of revenue from prohibited activity | Mixed-business companies can still fail |

| Speculative derivatives | Options-heavy strategies at fund level | Gharar and Maysir at the portfolio level |

Shariah-screened indices usually have fewer financial stocks and more technology stocks. For an AI-focused investment approach, this is not a limitation; it is actually an advantage.

However, many Muslim traders overlook an important detail. Even if an asset is perfectly screened, it becomes problematic if your broker charges overnight swap fees.

This is Riba, which is prohibited no matter what you are trading. A standard CFD account that charges interest on open positions brings in a prohibited element at the account level, even if the underlying stock is acceptable.

One solution is to use an Islamic account, also known as a swap-free account. These accounts remove overnight interest and replace it with either a fixed administration fee or a wider spread, though in binaries there’s often no direct spread charged. Though always check the actual fee schedule.

Bottom Line

IFG described prediction markets as “gambling with better branding.” The arguments based on Maysir, Gharar, and Qabd are strong, and the current platforms – offering disputed resolutions, supporting anonymous arbitration, and primarily serving retail speculation – do not provide a strong reason for an exception.

The hedging argument is valid, but it only applies if you have real underlying exposure. Most retail traders do not. Without that, you may fall under Mughalabat, no matter how well you have researched your position.

This debate will continue. Regulations are evolving, and Shariah advisory boards are still reviewing these instruments. The hedging use case may eventually become formalised.

For now, taking a careful approach is a reasonable choice, and the available alternatives are strong enough that you do not have to compromise your investment ideas.

Key Terms

- Maysir — Gambling. Wealth is transferred based on chance, with nothing productive created. The test isn’t whether risk exists – it’s whether the risk is the entire point of the transaction.

- Gharar — Excessive contractual uncertainty. Some may classify conditional future contracts as high-Gharar. The Polymarket dispute history illustrates why the concern is practical, not purely theoretical.

- Qabd — Legal or constructive possession. A related objection is that an event token may not represent ownership of a recognised asset, usufruct or service capable of valid exchange.

- Maslahah — Public interest. Permits flexibility where an instrument creates a genuine societal benefit. Prediction markets’ forecasting precision is the strongest argument here.

- Salam — An upfront-payment forward contract permitted in Islamic law. It is the basis for halal hedging and, conceptually, the closest thing in classical fiqh to a legitimate prediction-market trade.

- Mughalabat — Financial wagering. The OIC Fiqh Academy’s term for the speculative use of conditional contracts where no underlying exposure exists.

- Riba — Interest. In a trading context, this appears as swap fees on overnight positions. Islamic accounts remove it, but check the fee structure because some “swap-free” accounts simply rename it.

Further Reading

- Islamic Finance Guru — Specific analysis of Polymarket and Kalshi, published February 2026.

- IFG Fatwa Forum — Where Mufti Faraz Adam and others field specific Islamic-finance questions.

- Zoya — Shariah analysis of event contracts on Kalshi, Polymarket, and Robinhood.

- AAOIFI — International standard-setter for Islamic-finance Shariah compliance.

- OIC Fiqh Academy — Has issued resolutions on derivatives and risk-management contracts.

- BrokerListings.com — Tested and ranked swap-free broker accounts for Muslim traders.