Prediction Markets Arbitrage: Finding And Stress-Testing Edges

The arbitrage opportunity in an event contract you noticed probably isn’t real. The price gap might exist, but once you factor in the costs of closing both sides on two platforms, dealing with different order books, and having your money tied up for weeks until settlement, the advantage usually disappears.

This isn’t a guide to finding live arbs. It’s a guide to figuring out whether the one you think you’ve found is worth acting on.

Top Platforms For Prediction Markets Arbitrage

| Broker | Min Deposit | Expiry Times | ||

|---|---|---|---|---|

|

Crypto.com | Varies by payment method | 5 minutes to event cutoffs, can be hours, days and longer depending on contract | » Visit |

Crypto.com Prediction Markets

Crypto.com is a great choice for traders wanting to deal prediction markets on an intuitive app. Regulated by the CFTC, you can place simple yes/no bets on a wide range of events, from presidential elections to movements in the S&P 500, with contracts traded like shares. It doesn’t offer some of the advanced analysis tools and features of prediction markets platforms like IBKR’s ForecastTrader, but for mobile-first retail investors, Crypto.com is a user-friendly fit.

Visit

If You’re Coming From Binary Options

Binary options traders usually learn prediction markets quickly because the basic setup is familiar: buy a ‘YES/NO’ contract and collect $1 if you’re right. But there are some key differences in how arbitrage works, and missing these can lead to real losses.

The biggest difference is settlement. A binary option settles based on a broker’s price feed, using the mid-price of an asset at a set expiry time. Prediction markets settle based on real-world outcomes, which must be confirmed by a news source or an official body. When you arbitrage between two platforms, who confirms the outcome, and when they do, is critical. The 2020 election section later in this guide shows what happens when two platforms answer that question differently.

Counterparty matters too. In binary options, you trade against the broker, who sets the price and resolves the contract. In prediction markets, you trade against other people in a peer order book. This sounds simpler, but it means liquidity depends on what other traders are willing to offer.

Liquidity is often low regarding obscure events, sometimes decent for major elections or big sports finals, and unpredictable when you need to fill both sides of a trade quickly.

Regulation depends on the platform and where you live, including state-level differences in the US. For example, Kalshi is regulated by the CFTC in the US. Its main competitor, Polymarket, re-entered the US market legally after obtaining CFTC clearance through an acquisition, meaning it is no longer strictly “not available to US users,” though state-level restrictions still apply to several platforms.

Additionally, mainstream brokerages like Robinhood and TradeStation have integrated event contract trading directly into their retail platforms by routing orders through Kalshi’s backend infrastructure, permitting users to trade election, economic, and policy outcomes within traditional brokerage accounts.

Whether this is enforced is another matter, but the restriction exists. If your arbitrage strategy requires accounts on both platforms, make sure you can legally access them before you start.

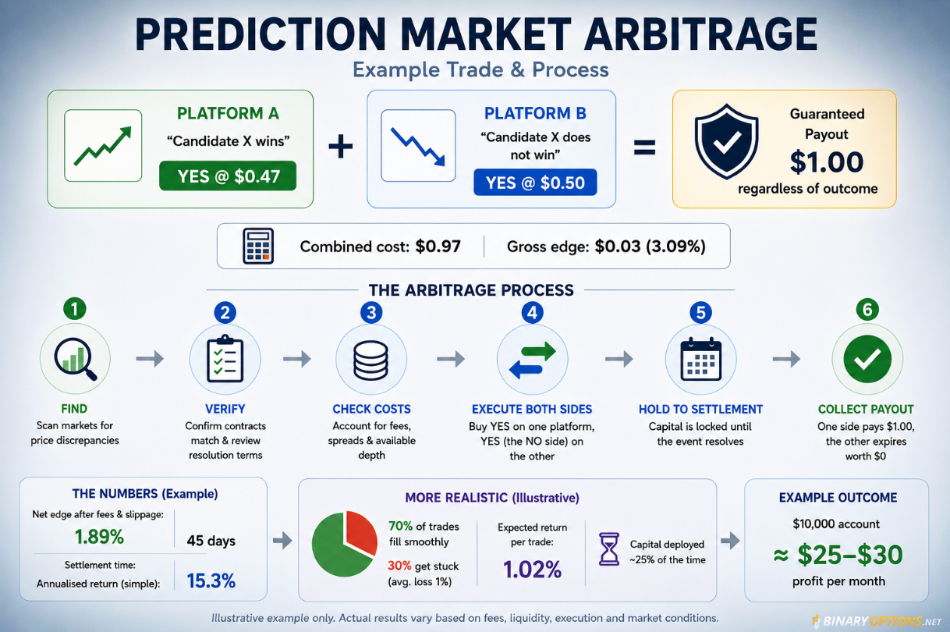

The Basic Maths

The simplest prediction market arb looks like this:

- Platform A: “Candidate X wins” YES at 48¢

- Platform B: “Candidate X does not win” YES at 49¢

- Combined cost: 97¢ → payout $1.00 → gross edge: 3¢

If both legs settle and they’re truly complementary, you’ve locked in a 3.09% return regardless of the result. Textbook arbitrage.

Here’s what usually ruins the opportunity. Platform fees are typically 2–5% of winnings on major prediction markets (can vary by market and venue), so a 3% gross edge can disappear or even turn negative before you’ve made any mistakes. Then there’s the bid/ask spread, which most arbitrage scanner tools don’t handle well – they show you the midpoint, not the actual ask price you pay.

Partial fill risk is another issue: one side fills, but the price changes on the other before you can close it, leaving you with a position you didn’t want. Even when everything goes smoothly, your 97¢ stays locked until the market resolves. For a contested political event, that could mean months.

That last point is often overlooked. While a 3% return might seem attractive, it translates to an annualized yield of approximately 12.4% if compounded four times per year. However, the opportunity cost becomes significant when the invested capital is locked for 90 days.

During this period, traders forgo the ability to allocate funds to alternative investment opportunities that may offer greater liquidity or higher expected returns, while simultaneously requiring continuous monitoring across multiple platforms and rapid responses to changing market conditions.

When ‘Arbitrage’ Is Not Arbitrage

- Most people think of cross-platform arbitrage as betting on the same event at two different places. Polymarket and Kalshi sometimes offer similar markets. However, fees, withdrawal rules, legal restrictions, and differences in contract wording mean that the “same event” isn’t always the “same contract.”

- Within-market sum arbitrage isn’t discussed as much. In a market with three or more possible outcomes, the YES prices should add up to about $1 minus the platform’s margin. If they don’t, like in a three-candidate race where YES prices total 94¢, there’s a theoretical edge. But in reality, these gaps close quickly once traders notice, and the amount you can trade at the mispriced level is usually very small.

- Combinatorial arbitrage happens when related markets suggest probabilities that don’t add up. For example, if “Democrats win Senate” trades at 60¢ and “Republicans win Senate” also trades at 60¢ in a two-party race, something is off. Quant traders with API access usually spot these before anyone looks manually.

- Latency arbitrage is an area where regular traders have little chance of succeeding. When news breaks, like a jobs report or a candidate dropping out, some markets update faster than others, creating a short-lived price gap. Academic research on Polymarket NBA markets found these opportunities last only seconds and are too small for most traders to benefit from. To take advantage of this, you need strong infrastructure, not just quick reactions.

7 Questions To Run Before You Trade

Most apparent arbs fail somewhere between questions three and five below. Running through all seven before placing a trade takes less than 10 minutes and saves a lot of grief.

- Are the two contracts describing exactly the same event, with the same resolution conditions?

- Do both platforms draw from the same source – the same oracle, the same news outlet, or the same official body?

- Is the full size you want to trade available at the quoted price, or is that the midpoint with $200 of depth behind it?

- After fees on both platforms, plus the bid/ask spread on both legs, does a positive return remain?

- If leg one fills and the price moves before leg two closes, what’s the loss?

- How long does capital stay locked, and what does that cost in terms of other opportunities?

- Are both platforms legally accessible from your jurisdiction?

What The Numbers Actually Look Like

Take a realistic example:

| Item | Value |

|---|---|

| YES cost — Platform A | $0.47 |

| NO cost — Platform B | $0.50 |

| Gross cost | $0.97 |

| Gross edge | 3.09% |

| Fees + slippage, estimated | 1.20% |

| Net edge | 1.89% |

| Settlement time | 45 days |

| “Annualised return” | 15.3% |

That 15.3% annualized return you see on most arbitrage calculators is very misleading. It assumes you can immediately reinvest your money as soon as a market settles, find another trade, execute both sides perfectly, and always have your capital available at the right time. In reality, things don’t work that smoothly.

A more realistic illustrative approach is to assume both sides of the trade fill smoothly 70% of the time. The other 30% of the time, one side gets stuck, losing about 1% on average. This brings the expected return per trade down to about:

(1.89% × 0.70) − (1.00% × 0.30) = 1.02%

Now consider that because capital is deployed only approximately 25% of the time – due to lock-up periods and the scarcity of viable opportunities – your effective rate of return is reduced accordingly.

For example, if a $10,000 account generates approximately a 1% expected return per trade and is active only one quarter of the time, the actual monthly profit is about $25–30, since most of the capital remains idle. This figure is above zero, but it is far from sufficient to constitute a sustainable or scalable business.

The traders who actually make money from prediction market arbitrage have automated both monitoring and execution, and they run these strategies across many markets at once. The real advantage comes from having the right systems, not just noticing a price gap online.

If you want to get started with automation, it makes sense to begin with basic scripting tools such as Python or Node.js. Both Polymarket and Kalshi provide public APIs that let you fetch live market and order-book data, and there are open-source libraries available to help with order execution and monitoring.

Even setting up simple scripts to pull data, check for price gaps, and send alerts to your phone or email is a practical first step before moving to fully automated trading. Over time, building on these tools can help you move toward end-to-end automation as your skills improve.

Why ‘Same Event’ Often Isn’t

Differences in contract wording cause more failed arbitrage attempts than fees do. Binary options traders often already have a good sense for this, since settlement language creates similar issues.

| Platform A wording | Platform B wording | The problem |

|---|---|---|

| “Will X win the election?” | “Will X be declared the winner?” | A contested result can split resolution timelines entirely. |

| “By December 31” | “Before December 31” | Not the same. What happens if the event falls on December 31 exactly? |

| Resolves via AP call | Resolves via official state certification | AP called Florida hours before state certification in 2000. |

| “Team X wins the championship” | “Team X is the champion” | A post-result disqualification could cause the contracts to resolve differently. |

| Three-outcome market: Win/Lose/Draw | Binary market: Win/Not win | “Not win” includes draws. “Lose” doesn’t. Your hedge may not be a hedge. |

These aren’t just rare exceptions buried in the fine print. They are the real terms employed in live markets on actual platforms, and they catch traders off guard all the time. Always read the resolution criteria on both sides before doing anything else.

What Happened In 2020

The clearest real-world example of resolution gap risk ran from November 2020 through January 2021.

On November 7, major US news networks called the presidential election for Biden.

Polymarket resolved its “Will Trump win the 2020 US presidential election?” market on November 9, once AP, The Wall Street Journal, and CNN had all called the race – the three sources named in its resolution criteria.

PredictIt did not resolve. It announced a settlement no earlier than January 6, 2021, when Congress met in joint session to certify the Electoral College result.

Fifty-eight days between platforms.

| Comparison | Polymarket | PredictIt |

|---|---|---|

| Resolution trigger | AP + WSJ + CNN call | Congressional certification |

| Resolution date | Nov. 9, 2020 | Jan. 6, 2021 |

| Days post-election | 6 | 64 |

Traders with a NO position on Polymarket collected their payout on November 9. Anyone whose hedge sat on PredictIt had capital frozen until January 6, during which time Trump contested the result, the PredictIt market kept pricing the uncertainty, and a neutral position started behaving like a live directional trade. The hedge dissolved. The capital stayed locked.

And this was predictable. The resolution criteria for both platforms were public. “Congressional certification” and calls from outlets like AP, WSJ, or CNN are prominently displayed at the top of each prediction market, so traders who made mistakes likely failed to review this primary information.

The Order Book Problem

Most arbitrage scanner tools display midpoint prices. The midpoint is the average of the best bid and the best ask, but it’s not the price you actually pay.

In a typical YES/NO contract, the best bid might be 47¢ and the best ask 51¢. The midpoint the scanner shows is 49¢. The price you pay to buy YES is 51¢. That’s a four-cent gap the tool didn’t flag, before a single fee.

Depth makes this problem worse. At 51¢, there might be $320 available, and the next price level is at 53¢. If your trade is larger than what’s available at the best ask, you end up paying more on average, and your edge gets smaller. In a cross-platform arbitrage, this occurs simultaneously across both order books, each having its own depth, fees, and execution limits.

At $2,000 in size on a modestly liquid market, most of the edge has gone.

Paper-Trading Before You Risk Capital

Before you risk any money on an opportunity, try paper trading for at least two weeks.

Get live order-book data using an API. Ignore the displayed price and record the best ask on both sides. Simulate executing both sides of the trade at those prices and at your intended size. Verify again after 30 seconds and five minutes to see if the spread persists. Keep a log of every opportunity you find, and note exactly why each one fails when you look closer. Over time, you’ll build a record of which market types, event categories, and platform pairs tend to produce false positives.

Most traders who engage in this paper-trading process observe that apparent price gaps seldom translate into profitable opportunities when simulated trades are executed at real market prices and intended sizes.

The main pitfalls identified include the rapid disappearance of price discrepancies due to limitations on order-book depth, the impact of platform fees, and the challenge of achieving full trade execution. Recognizing these limitations is essential before risking real capital.

Is Prediction Markets Arbitrage It Worth It?

For most traders, this probably isn’t a good main strategy. The costs are real, the profit margins are small, your money gets tied up, and actually executing trades is harder than it looks on a spreadsheet.

For traders with technical skills who can automate monitoring and execution across many markets, there is potential here. But this is more of a systems-engineering challenge than a trading one. You’re not manually searching for mispricings; you’re building systems to find and act on them faster than others.

Opportunities for prediction-market arbitrage do exist, but they are short-lived and constrained by costs such as fees and slippage. The 2020 election example is a good reminder that risks aren’t always about fees. Sometimes, your hedge can be stuck on one platform for months while the situation keeps changing.

FAQ

Can You Arbitrage Prediction Markets?

Yes, sometimes. Whether the edge survives fees, execution constraints, and settlement-timing differences is a separate question. For manual traders, usually no. For automated traders with fast execution and solid infrastructure, occasionally.

How Is Prediction Market Arb Different From Binary Options Arb?

Settlement structure is the main difference. Binary options resolve against a price feed the broker controls, so timing is predictable. Prediction markets resolve against real-world events confirmed by external sources – and when two platforms adopt different sources or different criteria, you get a situation like the 2020 example above.

What Kills Most Apparent Arbs Before Execution?

Fees first, then order-book depth. A 3% gross edge with a 2% fee on each leg is a break-even trade. Even when the edge survives on paper, the available size at the quoted price frequently falls short of what the trade needs to be worth running.

Are Arbitrage Finder Tools Any Good?

As a starting point for identifying candidates, they can be useful. As a signal to act, no. Most don’t account for order-book depth, platform fees, or distinct resolution criteria.