Binary Options vs Event Contracts: Is There Any Difference?

If you’ve ever traded binary options, your first look at a prediction market, also known as an ‘event contract’, will feel oddly familiar. The question is ‘yes’ or ‘no’. The payout is fixed. The clock is ticking. You either get it right or you lose your stake. That’s not a coincidence.

‘Event contract’ is the term that US regulators and a new wave of fintech platforms prefer. The CFTC uses it. Kalshi and Polymarket both use it. It sounds cleaner, more institutional, less associated with the offshore platforms that made binary options a dirty phrase in some Western financial regulatory circles. But strip away the branding, and you’re looking at the same fundamental structure: a time-limited, fixed-payout bet on a binary outcome.

To be fair, there are real differences. Regulation, market breadth, and settlement transparency genuinely separate some event contract platforms from the binary options world. Those differences matter, and we’ll cover them properly below.

But let’s be direct about what we think is also happening here: event contracts are, in large part, binary options repackaged with a cleaner design and a more palatable regulatory story. The fintech firms behind them are smart, well-funded, and very good at not looking like the binary options industry. That doesn’t mean the product is fundamentally different.

Binary Options vs Event Contracts: Feature Comparison

| Feature | Binary Option | Event Contract | Notes |

|---|---|---|---|

| Outcome structure | Yes/No | Yes/No | Structurally identical |

| Payout | Fixed (e.g. 0% or 100%) | Fixed (e.g. $0.00 or $1.00) | Same mechanic, different denomination |

| Underlying market | Mainly FX, indices, commodities, crypto | Financial events, elections, science, sport, culture | Event contracts cover far more ground |

| Expiry | Short – often around 30 seconds to a few weeks | Varies – minutes to months | Binary options skew much shorter |

| Regulation (US) | CFTC-regulated platforms exist like Crypto.com (e.g. acquired Nadex) | CFTC-regulated platforms exist (e.g. Kalshi) | Key difference on paper |

| Regulation (global) | Varies widely; many platforms are offshore | Still emerging; legally contested in several markets | Both have grey areas |

| Platform examples | Deriv, Pocket Option, IQ Option, Quotex | Kalshi, Polymarket, Manifold Markets, PredictIt | Different reputations |

| Exit before expiry | Available on some platforms | Kalshi allows early exit via live market | Worth checking per platform |

| Settlement authority | Usually the platform itself — often opaque | Typically a named third-party source (BLS, Federal Reserve, AP) | Biggest practical difference |

| Minimum trade size | Often $1 – $5 | Often $0.01–$1 | Event contracts can have a lower entry point |

| Pricing format | Payout percentage (e.g. “82% profit if correct”) | Probability price (e.g. Yes: $0.62 / No: $0.38) | Same information, different framing |

Most of the table should look familiar if you’ve traded binary options. The real divergence sits in three rows: regulation, settlement authority, and market breadth. Everything else is close enough that you’d need to look twice.

The Payoff Is Similar – A Side-By-Side Walkthrough

The best way to show how similar these products are in practice is to test them on the same event.

We ran this comparison ahead of a US Consumer Price Index (CPI) release – one of the most-traded economic events in both markets – using Kalshi for the event contract side and Pocket Option for the binary option side. Here’s what we found.

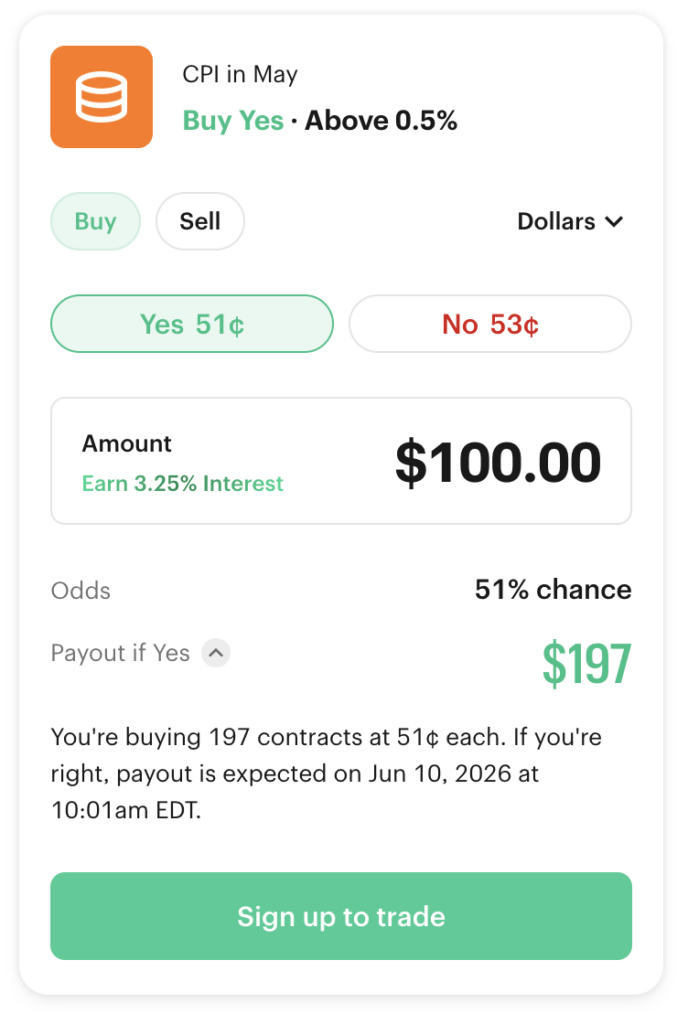

The event contract (Kalshi):

“Will CPI come in at or above 0.5% for the month?”

Yes contracts: $0.51 | No contracts: $0.53

Kalshi priced Yes at 51 cents – implying a 51% market probability that CPI hits that level. Buy 10 Yes contracts for $5.10. If CPI prints at or above 0.5%, each contract pays $1.00. Total return: $4.90 profit on $5.10 staked. If you’re wrong, you lose the $5.10.

The settlement source is listed on the contract page: the Bureau of Labor Statistics official release. No ambiguity about who calls it.

The binary option (Pocket Option):

“Will USD/JPY be above 153.40 at 8:35am EST?”

Payout if correct: 75% | Loss if wrong: 100% of stake

Set a $10 trade. If USD/JPY is above 153.40 at expiry – a few minutes after the CPI number drops and the dollar moves – you collect $17.50 (your $10 back plus $7.50 profit). If you’re wrong, you lose the $10.

The framing is different. One asks about an economic data point directly; the other asks about a currency pair that will react to it. But the decision you’re making is functionally the same: which way does this go when the number hits at 08:30 EST?

What the order tickets show:

On Kalshi, the order screen shows the number of contracts purchased, the price per contract, and the maximum profit – but the total loss isn’t called out. It’s implied by the total cost (that’s what you lose if you’re wrong), but it’s not explicitly labeled. Everything else is fixed before you confirm.

On Pocket Option, the trade panel shows your stake, the payout if correct, and a countdown to expiry – the potential loss isn’t displayed separately, since you simply lose whatever you staked. Same information, different layout.

Cover the platform logos, and you’d struggle to tell them apart. That’s not an accident – it’s what the same product mechanic looks like when two different industries build a UI around it.

The one thing that does look different: Kalshi’s contract page links directly to the BLS as the settlement source. Pocket Option’s trade ticket shows a payout percentage and an expiry time. There’s no named source for the price at expiry. That gap matters more than the rest of the differences combined.

Why Binary Options Traders Will Feel At Home

If you’re coming from binary options and looking at event contracts for the first time, the learning curve is minimal. Here’s why:

- Fixed risk/reward. You know what you can win and what you can lose before you click. No stop-losses, no margin, no slippage. The worst case is your stake. That’s a feature, not a limitation, for traders who want defined exposure.

- Yes/no decision. You don’t need to forecast how much something moves. Just whether it does. That simplicity is why both products attract new traders – and why they can also encourage overtrading.

- Probability-style pricing. Contracts priced between $0 and $1 on Kalshi are expressing an implied probability. A Yes contract at $0.65 means the market thinks there’s a 65% chance it happens. Binary options traders think this way already, even if their platforms don’t label it explicitly.

- Time-based expiry. Every contract has a hard deadline. The trade lives or dies at a specific moment. Binary options traders are used to this rhythm.

- Short-duration options. Many event contracts settle within hours or a day. Some run longer, but there are enough short-duration contracts in the economics and finance categories to feel familiar.

- No ownership of the underlying. You’re not buying dollars, gold, or anything else. You’re taking a position on an outcome. Same as a binary option.

The cognitive load of switching between these products is low. That’s relevant for traders. It should also be relevant for regulators watching where binary options traders go next.

Where Event Contracts Are Actually Different

We’ve been critical of the repackaging narrative, but it’s worth being precise about where event contracts genuinely differ.

Regulatory Oversight – At Least In Theory

Platforms like Kalshi and the North American Derivatives Exchange (Nadex) operate under strict oversight by the US Commodity Futures Trading Commission (CFTC). That’s a real distinction. It means audited financials, segregated client funds, formal dispute processes, and regulatory accountability that the offshore binary options world simply doesn’t have.

Polymarket is legal at the federal level in the US following CFTC approval and the launch of a regulated US platform. However, the US version is highly restricted – limited to a narrower range of event contracts, such as sports and politics.

The legal status in Europe remains highly fragmented. For example, regulatory authorities in countries like Spain, France, and the Netherlands have taken strict stances, temporarily banning major platforms from operating in their jurisdictions for lacking local mandatory gambling licenses.

The UK’s approach is entirely different; regulators generally classify prediction markets as betting exchanges. Therefore, any legal prediction market must operate under a gaming or betting license. Matchbook, for example, launched the UK’s first licensed prediction market platform.

But regulated doesn’t mean safe, and it doesn’t mean profitable for retail traders. CFD and options data consistently show 70–80% of retail traders lose money across products with similar structures. Event contracts are new enough that comparable retail loss data hasn’t yet been published. When it is, we expect similar numbers. Regulation changes the legal environment. It doesn’t change the math of fixed-payout trading.

Market Breadth Goes Well Beyond Finance

This is the biggest practical difference. On Kalshi, Polymarket, and Manifold, you can trade on elections, Fed decisions, CPI releases, scientific study outcomes, award show results, and more. Some platforms include sports markets – though those are legally contested in many US states.

For binary options traders, this expansion sounds appealing. More markets mean more opportunities. But it also means trading on things you may know nothing about. You might have an edge in forex markets, but zero edge in congressional approval polls or box office forecasts. The breadth of event contracts isn’t a risk-free upgrade. It’s more rope.

Settlement Transparency

As we showed in the walkthrough above, event contracts from regulated platforms typically tie settlement to a named, independent data source. The contract specifies who calls the result and where that data comes from. That’s a meaningful improvement over the binary options world, where settlement prices have historically been determined by platform data feeds with limited transparency – and where disputes have been common.

This isn’t a marketing difference. It’s a structural one. If you don’t know who settles a contract, you don’t fully know what you’re trading.

How Binary Traders Should Approach Event Contracts – A Practical Checklist

Don’t assume a CFTC-regulated label means a problem-free trade. Here’s what to verify before you commit money to any event contract platform or specific contract.

1. What Exactly Determines Settlement?

Read the contract specification, not just the headline question. “Will CPI beat expectations?” raises several follow-up questions: whose expectations? Which CPI measure? What happens if the number is revised after initial release?

On Kalshi, this information is in the contract details tab – it’s explicit. On other platforms, it may not be. If you can’t find a clear settlement rule, don’t trade the contract.

2. Who Is The Settlement Authority?

Is settlement determined by the platform itself, a named data source, or an independent resolution council? Third-party resolution is more trustworthy than platform-resolved, for the same reason you’d rather have an independent auditor than a company marking its own homework. Check whether there’s an appeal mechanism and how long it takes to resolve.

3. What Happens If The Event Is Delayed, Canceled, Or Disputed?

This varies significantly by platform, and it’s genuinely underreported in most event contract guides. Some platforms void the contract and return stakes; others hold it open until the event occurs. Kalshi has documented resolution rules for delayed events. Others are less clear. Read the terms before you trade. This is the question most traders ask only after something goes wrong.

4. Can You Exit Before Expiry?

Kalshi allows early exit – you can sell your contract back into the market at the current price. Most binary options platforms don’t offer this; once you’re in, you’re in until expiry. Early exit is a significant risk management tool. Know whether you have it before you size a trade. If you’re trading on a platform that doesn’t allow it, treat every position as if it must run to expiry.

What This Means For Binary Options Traders

Don’t assume event contracts are automatically safer just because a regulated US platform offers them. The trade mechanic is the same as binary options: fixed outcome, fixed payout, time-limited, and you either get it right or you lose your stake. The “event contract” framing comes with better branding and, in some cases, better regulation.

But the core risks haven’t changed. Poor contract interpretation, overtrading, and stepping into markets where you have no edge will cost you money on Kalshi just as fast as on an offshore binary options platform.

The expansion beyond financial markets makes that risk worse, not better. Binary options traders are used to currency pairs and indices. Event contracts now span elections, cultural events, science outcomes, and more. That’s a genuinely different type of trading – and most people moving from binary options to event contracts aren’t treating it like one.

A CFTC-regulated venue is better than an offshore platform with no accountability. That’s true, and it matters. But it’s not a substitute for understanding exactly what you’re trading, who settles it, and whether you have any real edge in that market.

Event contracts are binary options with a cleaner story. Whether that story holds up depends less on the platform and more on the trader.