Some more vertical spreads

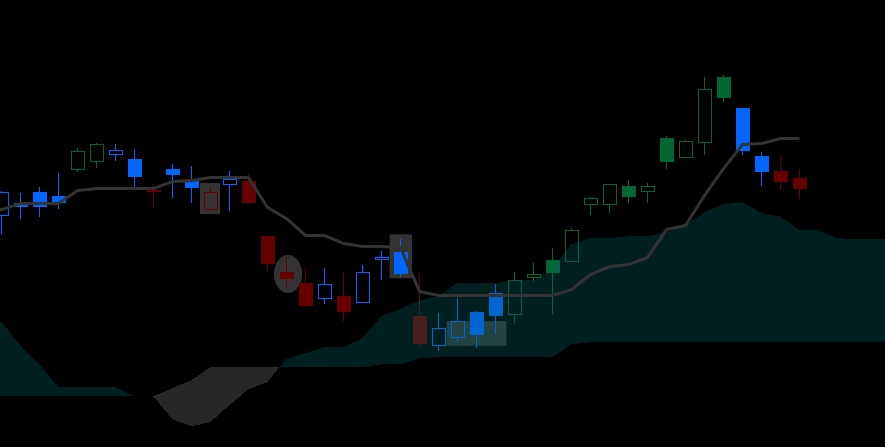

In my previous post I set up a vertical spread in SPY at end of day 8/12, the leftmost highlighted day on this chart.

If you look back to the risk graph of either vertical you’ll see a line at 171, that’s because I want to be able to hedge most losses up to that point. During option trading hours I would close the spread well prior to that, but I want to be sure I can hedge in a bad case scenario. At a quick move to 171 (recent highs) the position would lose about $800. That’s about a 2-point SPY move & about 20 ES points.

Putting it together, if this trade goes quickly against me (when the options market is closed) I should be able entirely hedge the spread with one ES futures contract. Catching only 1/2 the move amounts to losses of about $300 per $3,000 margin when hedging with 1 ES contract. So that’s about $300 loss per 7k dedicated, or roughly 4%.

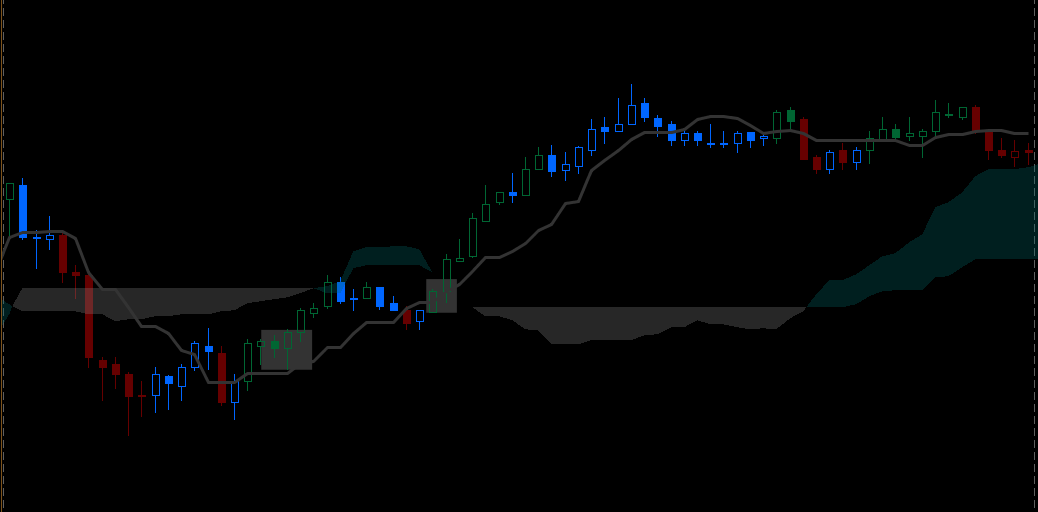

The day after entering the position is an up day and the spread is down about $100. Following are two 5 minutes charts of that next day, 8/13. The first is the ES and the second is a graph of an SPY call option with 3 days until expiration.

Note that in this case it wasn’t hard to get 8 to 10 points in the ES, meaning somewhere around $450 profit from actively hedging. Most days it’s not so easy to get so much from the ES, but most days don’t hurt the spread either – I’m only trading very clear moves when hedging. The option graph moved in a very similar way, but the leverage is entirely different. Each option cost around $70 at entry and was worth about $115 as price flattened out. That’s a return of about 60% on margin compared to about 11% for the ES. In this case I would stop the hedge trade at about $15 loss per option, 2% of 7k / 15 is 10 so 10 options would be about right and the hedge would have profited about $450 – roughly the same dollar amount as the ES hedge but with 1/5 the margin.

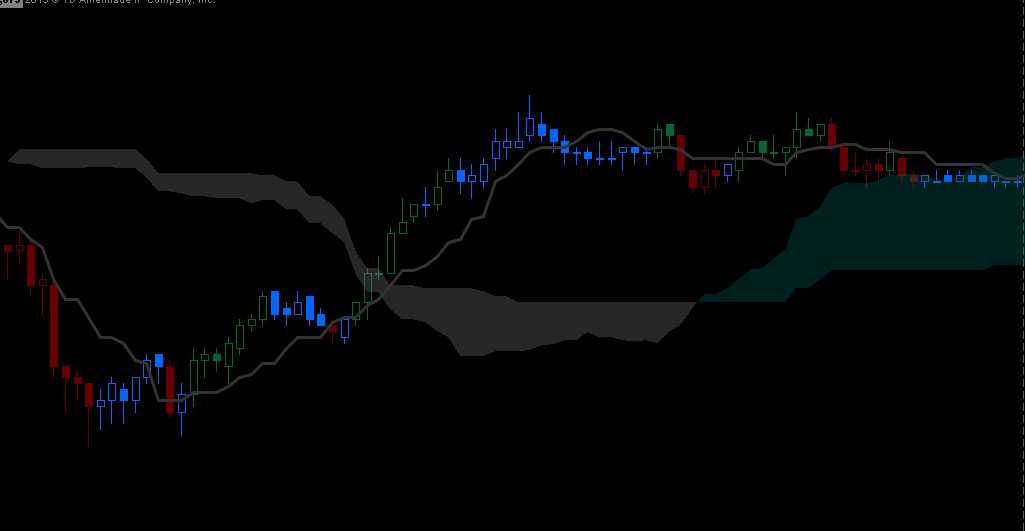

End of day Friday, 8/16 the spread looks great & I would remove it rather than hedge the weekend. If you still like the spot a new position probably offers better risk reward. I don’t like to morph positions, there are wide variety of ways to restructure an options position along the way but I prefer to keep it simple – my expectation has occurred & the spread made good money, take the profit.

This position was constructed looking backward & obviously worked out very well. However the original assumption was very reasonable & risk to the account was never more than 4%, probably not even that. The point is that by using index options an already skilled trader can construct potentially large payoff positions with reasonable risk. In this case add 2 successful hedge days to the profit from the spread and the position profited roughly one third of the account.

In the next post I’ll illustrate an options position known as a Butterfly & see why it makes sense for 8/19, the Monday following the close of the verticals.